welfare.

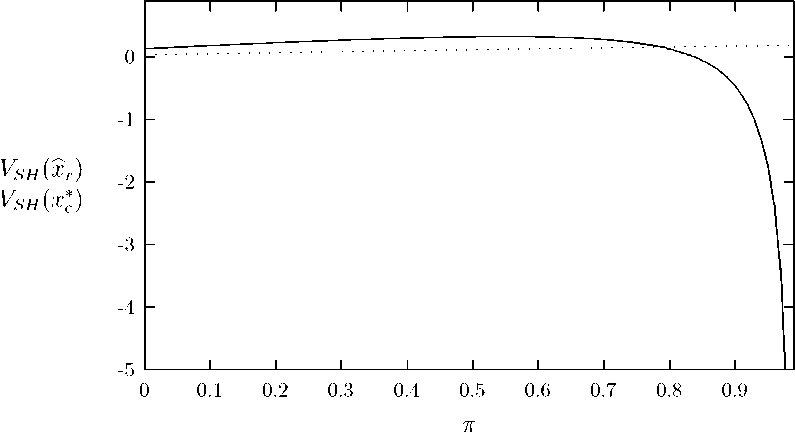

Example 1 In figure 3 we set θI = .1, θR = .5, α = .5, p = .5, τ = .5, λ = .7, a = .4, B = 2

and Γ = 0.8. With these parameters π* = 0.44 and br(π*) = 0.47 .

Example 2 In figure 4 we keep the same data of example 1 but assume that both the

stakeholder ability at affecting the replacement decision, and the incumbent control benefits

are higher (i.e. we set a = .8 and Γ = 2). In this case: π* = 0.038 and br(π*) = 0.063.

Figure 3: The continuous (dotted) curve represents shareholder value when entrenchment is

(not) to be countered. Shareholders preempt entrenchment: π* = 0.44 and xbr(π*) = 0.47.

Notice that in both examples shareholder value is indeed maximized by countering man-

agerial entrenchment (i.e., it is not optimal to set π and xr below the xbr(π) locus). Therefore,

we can conclude:

Proposition 2 There is an open set of parameters for which shareholder value is maximized

by countering managerial entrenchment, and hence by providing a minimal level of explicit

stakeholder protection xbr (π*) > 0.

Remark 2 — Welfare effects — To be written.

17

More intriguing information

1. The East Asian banking sector—overweight?2. What should educational research do, and how should it do it? A response to “Will a clinical approach make educational research more relevant to practice” by Jacquelien Bulterman-Bos

3. IMPROVING THE UNIVERSITY'S PERFORMANCE IN PUBLIC POLICY EDUCATION

4. Strategic Planning on the Local Level As a Factor of Rural Development in the Republic of Serbia

5. Voting by Committees under Constraints

6. The name is absent

7. Importing Feminist Criticism

8. Optimal Private and Public Harvesting under Spatial and Temporal Interdependence

9. Globalization, Redistribution, and the Composition of Public Education Expenditures

10. Ultrametric Distance in Syntax