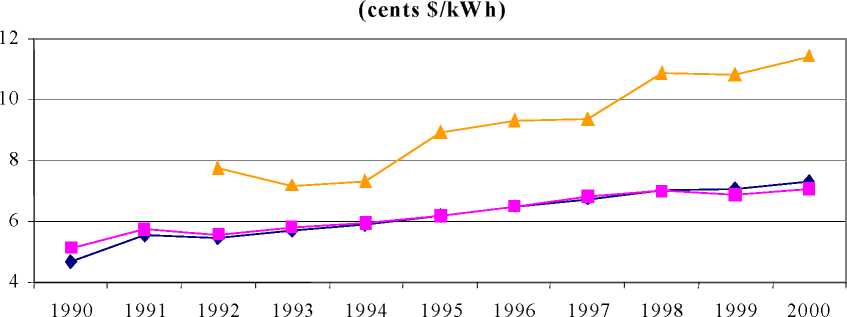

Figure 3.8

Average National Tariff by Groups of Operators

G— Group 1

fl— Group 2

G— Group 3

Source: Superintendency of Electricity

Figure 3.8 above shows that Groups 1 and 2 experienced basically the same evolution of tariffs

over the period analyzed. Group 3 operators on the other hand, serving rural and poorer Bolivia,

experienced a significant increase of tariffs between 1992 and the year 2000. In all, Group 3‘s

tariffs increased by 47% between the two end years, whereas Group 1‘s and Group 2‘s tariffs

increased, respectively, by 34% and 28%.

One reason for the overall increase in tariffs is that Bolivia’s electricity industry, like others in the

world, has been characterized by cross-subsidization schemes that were to be phased out after the

passage of the electricity law in 1994. In reality and since 1994, some reduction on the levels of

cross subsidization has indeed occurred, though it is still widely used to ensure cheaper prices for,

basically, residential consumers. With the gradual phasing out of cross subsidization, it should

come as no surprise that those areas with comparatively larger residential consumers and smaller

or non existent commercial activity, would also be the ones with the deepest increases in rates,

since subsidization from the latter to the former is decreasing. The observed pattern of behaviour

of tariffs illustrated in figure above seems to follow that line of reasoning.

A somewhat clearer picture on prices due to less cross subsidization is observed when prices for

different categories of consumers are plotted for different operators serving different

departments. It would be expected that as subsidization is phased out, prices for the subsidized

category would begin to increase while prices of those categories utilized to subsidize other

sectors would fall. Figure 3.9 below shows time-series price data corresponding to electricity

Elfeo (Oruro), Cessa (Chuquisaca) and Sepsa (Potosi). Group 3 includes all rural operators within the National

Interconnected System (NIS).

17

More intriguing information

1. Testing Gribat´s Law Across Regions. Evidence from Spain.2. Linking Indigenous Social Capital to a Global Economy

3. Stillbirth in a Tertiary Care Referral Hospital in North Bengal - A Review of Causes, Risk Factors and Prevention Strategies

4. Urban Green Space Policies: Performance and Success Conditions in European Cities

5. Psychological Aspects of Market Crashes

6. ALTERNATIVE TRADE POLICIES

7. The name is absent

8. Understanding the (relative) fall and rise of construction wages

9. The name is absent

10. The name is absent