intercept in the cointegration space combines with the intercept in the short run model

resulting in an overall intercept contained in the short-run model; (M4) if there exists an

exogenous linear growth not accounted for by the model, the cointegration space includes

time as a trend stationary variable.

Because usually is not known a priori which model to apply, the Pantula principle (Harris

1995) is used to simultaneously test for the model and the cointegration rank.

4. Data and results

The theoretical model developed by Saghaian et al. (2002) serves as a guide for our empirical

work. This model supposes a small open economy which is an appropriate assumption for

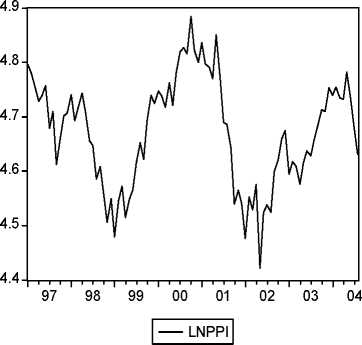

Hungary. Monthly time series of an agricultural variable, the log of producer price index

(lnPPI), the log of industrial producer price index (lnIPI), the log of Euro/Hungarian Forint

exchange rate and the log of the seasonally adjusted money supply (M1A) were used. The

dataset presented on figures 1 and 2, covers the January 1997 - August 2004 period,

consisting of 92 observations. Data sources are the CSO-Central Statistical Office, and NBH

- National Bank of Hungary.

Figure 1. The logs of agricultural producer and industrial producer price indexes

4.84

4.56

I-----LNIPI I

97 98 99 00 01 02 03 04

More intriguing information

1. Popular Conceptions of Nationhood in Old and New European2. PEER-REVIEWED FINAL EDITED VERSION OF ARTICLE PRIOR TO PUBLICATION

3. Towards Teaching a Robot to Count Objects

4. The name is absent

5. The name is absent

6. Non-causality in Bivariate Binary Panel Data

7. The name is absent

8. The name is absent

9. The name is absent

10. The name is absent