11

5. Spatial autocorrelation

In advance to estimation und testing Moran’s I is computed as an overall measure for

spatial autocorrelation for the variables considered. For the Okun relation, the FD speci-

fication is preferred, as it is based on observables. For all variables, the Moran coeffi-

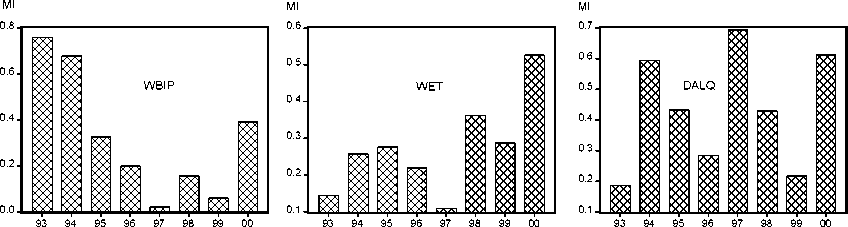

cient fluctuates over time (see Figure 5.1). However, in most years spatial dependencies

are striking in every case. With the exception of GDP growth in 1997 and 1999,

Moran’s I is significant at least on the 5 per cent level.2

As spatial autocorrelation varies over time, it will be not be removed by uniformly ap-

plying Griffith’s filtering method to the variables over the entire sample period. This

view is supported by the distinct map patterns in individual years. Although some

common spatial components of the variables are at work over time, other eigenvectors

of the C matrix change their significance from year to year. Hence, a varying spatial

pattern has to be taken into account.

Figure 5.1: Moran’s I of georeferenced variables

GDP growth Employment growth Unemployment (FD)

The spatial SUR model (3.4) presupposes that the explanatory variable is independent

from the error term.3 Thus GDP growth is pre-filtered to remove spatial effects. The

growth rate of employment and the change of the unemployment rate are explained by

the spatially filtered GDP growth rate and the map patterns of the endogeneous vari-

ables, that are extracted from the C-matrix. The spatial autocorrelations of the candidate

2 The significance of Moran’s I holds for both approaches randomisation and normal approximation.

3 The issue of exogeneity of output in Verdoorn’s hypothesis is addressed by Fingleton (2000) in a spatial

lag model. Though the Hausman test provides some evidence for endogenous output, due to indetermi-

nateness Fingleton favours output to be treated as exogenous.

More intriguing information

1. A Brief Introduction to the Guidance Theory of Representation2. Demand Potential for Goat Meat in Southern States: Empirical Evidence from a Multi-State Goat Meat Consumer Survey

3. The Impact of Financial Openness on Economic Integration: Evidence from the Europe and the Cis

4. Campanile Orchestra

5. Altruism with Social Roots: An Emerging Literature

6. The name is absent

7. Linkages between research, scholarship and teaching in universities in China

8. The name is absent

9. Peer Reviewed, Open Access, Free

10. Making International Human Rights Protection More Effective: A Rational-Choice Approach to the Effectiveness of Ius Standi Provisions