rate is trendless in the long-run. In general, equilibrating mechanisms in the labour market

and other markets are jointly responsible for this phenomenon. Thus restrictions on the

relationships between the long-run growth rates (as opposed to the levels) of capital stock

and other growing exogenous variables are sufficient for this purpose.

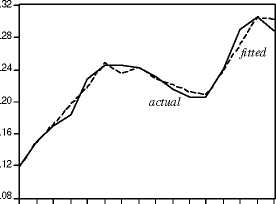

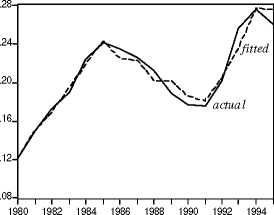

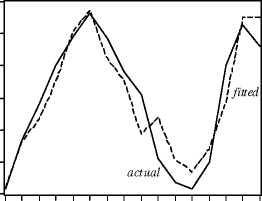

Figure 2 shows that the fitted unemployment rate generated by our system tracks the

trajectory of the actual unemployment rate very accurately.

In the following sections we seek to examine the role played by the lagged adjustment

processes and their interplay with the changes in the exogenous variables in the evolution

of the unemployment rate.

a. High unemployment regions

1980 1982 1984 1986 1988 1990 1992 1994

c. Aggregate unemployment rate

Figure 2. Actual and fitted values

b. Low unemployment regions

1980 1982 1984 1986 1988 1990 1992 1994

.24

.22

.20

.18

.16

.14

.12

5 Persistence of Shocks

We first show that the set of lagged adjustment processes in the model and their interplay

with the feedback mechanisms give rise to the propagation of shocks. In the context of

the estimated models in Tables 5 and 6, we measure the impacts of the different labour

market shocks on the time path of the unemployment rate for the two groups of regions.

Following the methodology outlined in section 2, we derive the reduced form unem-

ployment rate equation for each group of regions

ρ (L) uit = b (L) xit + c (L) zt + θd (L) εint + θw (L) εiwt + θs (L) εlit, (18)

where the autoregressive polynomial ρ (L) is dynamically stable,36 xit is a 3 × 1 vector

of exogenous regional variables and zt is a 4 × 1 vector of exogenous national variables;

b (L) and c (L) are 1 × 3 and 1 × 4 vectors of lag polynomials, respectively; εint , εiwt , and εlit

are the error terms in the labour demand (employment), wage setting, and labour supply

(labour force) equations, respectively, given in Tables 5-6. Note that the parameters in all

of the above lag polynomials - autoregressive ρ (∙), slope b (∙), c (∙), and moving average

θ (∙) - are functions of the estimated coefficients given in Tables 5-6.

36 Note that ρ0 = 1 so that ρ (L) = 1 + ρ1L + ... + ρqLq. Dynamic stability implies that the roots of

ρ (L) = 0 lie outside the unit circle.

16

More intriguing information

1. The name is absent2. The Triangular Relationship between the Commission, NRAs and National Courts Revisited

3. Langfristige Wachstumsaussichten der ukrainischen Wirtschaft : Potenziale und Barrieren

4. BODY LANGUAGE IS OF PARTICULAR IMPORTANCE IN LARGE GROUPS

5. The bank lending channel of monetary policy: identification and estimation using Portuguese micro bank data

6. Tariff Escalation and Invasive Species Risk

7. A Brief Introduction to the Guidance Theory of Representation

8. BUSINESS SUCCESS: WHAT FACTORS REALLY MATTER?

9. Poverty transition through targeted programme: the case of Bangladesh Poultry Model

10. The name is absent