Liguria) and in “area 5” (Abruzzi, Molise, Puglia and Basilicata). In all the other cases, there is no precise

pattern (at least without using econometric methods) between the lender size and the level of the interest

rates. This means that there seems to be no precise link between the lenders size and their market power.

For this reason, other variables, different from the lender size are employed in the econometric analysis as

proxies for the lender’s market power, in particular, as shown in section 4.1, we employ the spread

between maximum lending rate and minimum borrower’s rate for each class size and in each geographic

area.

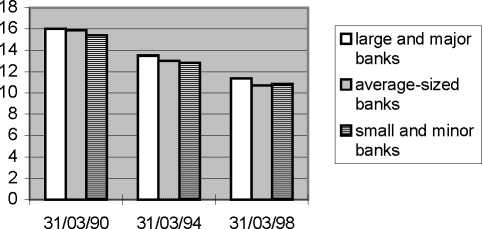

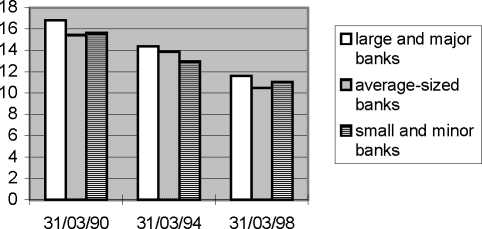

Lending rates to loan size class “c3” in area 1

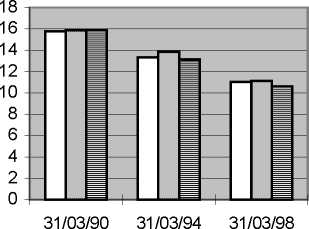

Lending rates to loan size class “c3” in area 2

□ large and major

banks

□ average-sized

banks

□ small and minor

banks

Lending rates to loan size class “c3” in area 3

More intriguing information

1. The name is absent2. An Empirical Analysis of the Curvature Factor of the Term Structure of Interest Rates

3. The name is absent

4. Education Responses to Climate Change and Quality: Two Parts of the Same Agenda?

5. The name is absent

6. Effects of a Sport Education Intervention on Students’ Motivational Responses in Physical Education

7. The Impact of Optimal Tariffs and Taxes on Agglomeration

8. Trade and Empire, 1700-1870

9. Pupils’ attitudes towards art teaching in primary school: an evaluation tool

10. The duration of fixed exchange rate regimes