A THEORETICAL GROWTH MODEL FOR IRELAND

257

of capital with respect to investment of 0.3. Finally, we set r* = 0.05 and using

evidence on the sensitivity of interest rates to external debt from Lane and

Milesi-Ferretti (2001), we assume that (a) the elasticity of Φ(K) is equal to .01

and (b) the debt related risk premium is 2 per cent.

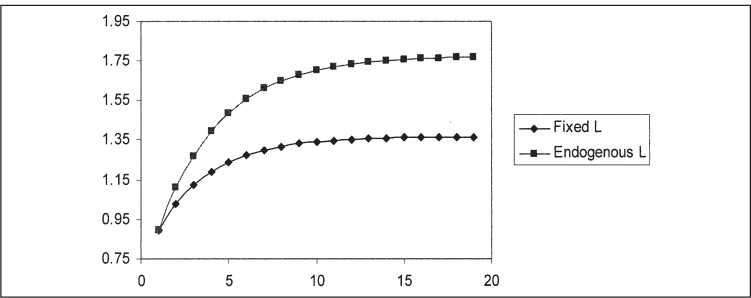

Figure 4 illustrates the role of labour market openness in the growth

process. In the Figure, we compare two alternative convergence processes,

where in one case, the labour force is constant throughout, and in the second

case, employment responds endogenously to capital accumulation through the

process described in Equation (8). In both cases, we have set the initial capital

stock equal to 30 per cent of its steady state level, so that initial GDP is below

steady state GDP.13 As we can see from the Figure, the channel of endogenous

employment expansion during the growth process implies a higher steady

state GDP and a much higher growth rate during the convergence, beginning

from an initial low level of GDP. As capital accumulation takes place,

beginning from an initial low capital stock, the real wage in the home economy

rises, drawing in labour from outside, magnifying the process of accumulation

itself.

Figure 4: Labour-Market Openness and Growth

Figure 5 illustrates the role of international capital markets. The Figure

again shows the convergence process, beginning from an initial capital stock

equal to 30 per cent of steady state capital, but now contrasting the baseline

calibration against a case where the opportunity cost of borrowing is sharply

rising in foreign debt - we set the elasticity of the function Φ(K) equal to unity.

This implies a much higher degree of restrictiveness of international capital

markets. Again we see that capital market openness is a critical feature of the

convergence process, in the same way as is labour market openness. With

13Figures 4 and 5 have time in years on the horizontal axis and an index of GDP on the vertical.

More intriguing information

1. The name is absent2. Education and Development: The Issues and the Evidence

3. The name is absent

4. The Functions of Postpartum Depression

5. Banking Supervision in Integrated Financial Markets: Implications for the EU

6. Palvelujen vienti ja kansainvälistyminen

7. Measuring and Testing Advertising-Induced Rotation in the Demand Curve

8. For Whom is MAI? A theoretical Perspective on Multilateral Agreements on Investments

9. The name is absent

10. Are Japanese bureaucrats politically stronger than farmers?: The political economy of Japan's rice set-aside program