William Davidson Institute Working Paper 402

1+b+d

m = M/B =-------- > 1.

r+b+ρd

It can be seen that the multiplier is a decreasing function in b, r and ρ. That

means that, ceteris paribus, increases in the reserve ratios would reduce the money

stock. An increase in the public propensity to hold cash would also reduce the money

stock. The impact of increased propensity to hold dollar denominated deposits is more

ambiguous. The sign of the derivative:

∂m _ b(1 - ρ) + (r - ρ)

Idd ~ (r + b + ρd)2

is clearly positive if r≥ρ, that is if the reserve ratio that applies to deposits in lei is

larger than the reserve ratio that applies to dollar (and euro) deposits. Since August

1998 this condition is clearly fulfilled as the minimum reserve ratio were around 30%

for lei and 20% for dollars (in July 2001, r=27% and ρ=20%).

This configuration brings about additional volatility. If, for some reason,

people lose confidence in the domestic currency, they would shift to dollar

denominated deposits (d increases). This would raise the multiplier and the money

supply, and would entail a decline in interest on lei deposits, which would ex-post

validate the adverse “confidence” shock. On the contrary, if ρ>(r+b)/(1+b)>r, then

the increase in the propensity to hold dollar deposits may have a stabilising effect in

the event of credibility shocks.

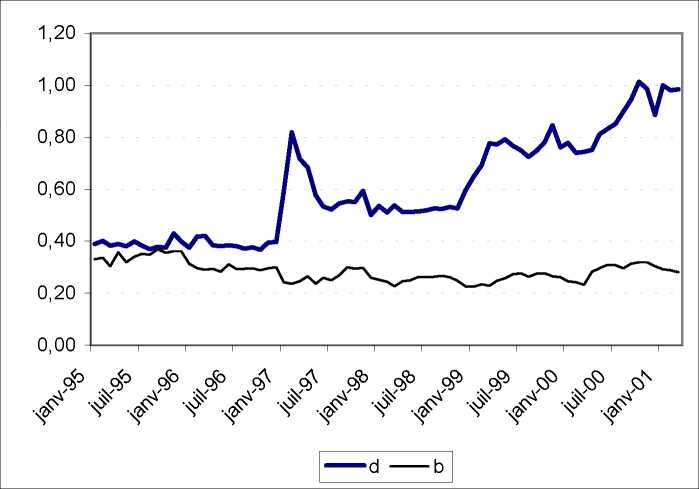

The figure below depicts the time patterns of the ratios b and d.

Figure 5. Propensity to hold cash and dollar deposits. January 1995 to March 2001.

Here b is the ratio of cash outside banks to total lei deposits and d is the ratio of dollar

deposits (expressed in lei) to total lei deposits. Source: NBR, Monthly statistical bulletins

and own calculations of the authors.

It can be seen that the propensity to hold lei in cash is rather stable after 1997,

fluctuating around 0.25. But the propensity to hold dollars has increased markedly,

16

More intriguing information

1. An Efficient Secure Multimodal Biometric Fusion Using Palmprint and Face Image2. The name is absent

3. Testing Panel Data Regression Models with Spatial Error Correlation

4. Migration and employment status during the turbulent nineties in Sweden

5. Visual Perception of Humanoid Movement

6. Washington Irving and the Knickerbocker Group

7. The name is absent

8. The name is absent

9. Proceedings from the ECFIN Workshop "The budgetary implications of structural reforms" - Brussels, 2 December 2005

10. Linking Indigenous Social Capital to a Global Economy