William Davidson Institute Working Paper 402

During the 1999 crisis, the NBR, instead of raising interest rates, bough lei

massively (and sold reserves, as shown in Figure 7). This may have limited the size of

the devaluation, but at the cost of a rising default risk on foreign debt due to reserve

depletion.

9. More empirical evidence on the devaluation - inflation relationship

Let us consider more in depth the factors that contributed to the steady

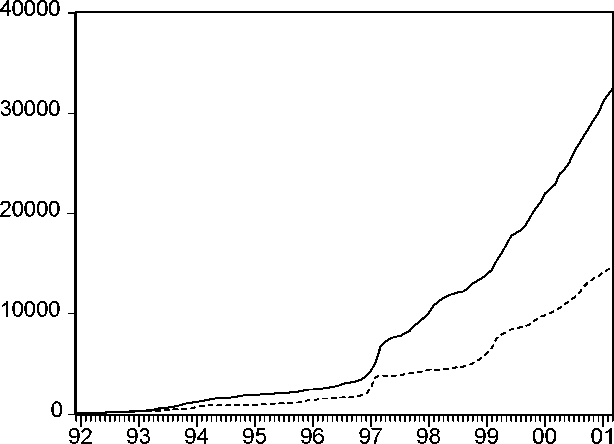

nominal devaluation of the leu. In Figure 9, it can be seen that the nominal exchange

rate has evolved in pair with prices in the goods market.

---CPI -----Exchange Rate Index

Figure 9. Nominal exchange rate and CPI Indexes (base 100 in December 1991).

January 1992 to March 2001. Source: NBR

But has the leu depreciation been a major cause of price inflation or, as

elementary monetarist logic would imply, the nominal devaluation only reflects, with

a lag, the price increase? A Granger causality test tends to corroborate the former

hypothesis, indicating that exchange rate hikes lead the rise in prices. But the

monetarist logic is not completely falsified. A similar test run this time on inflation

and money growth rate shows that the money growth rate also leads the price increase

(see Appendix A for the two tests).

Of course, a theory of inflation for economies with a distorted microeconomic

structure and lack of basic institutions like the Southeast European ones is difficult to

work out. Therefore we limit ourselves to a basic empirical approach and develop a

simple VAR model, considering the interplay between changes in prices, changes in

the money stock and changes in the nominal exchange rate. Data are monthly, in the

interval 01:1997 to 03:2001. We did not consider earlier data, as the exchange rate

was not fully liberalized. Equations of the model are presented in the Appendix.

The response of the inflation rate to a shock in the money growth rate (DRM)

and in the devaluation rate (DVN) is depicted in the figure below. As can be seen, a

one standard deviation impulse in the former variables entails significant inflation

acceleration (up to 1.5% per month inflation increase). The maximum impact is

22

More intriguing information

1. Return Predictability and Stock Market Crashes in a Simple Rational Expectations Model2. Firm Closure, Financial Losses and the Consequences for an Entrepreneurial Restart

3. Implementation of Rule Based Algorithm for Sandhi-Vicheda Of Compound Hindi Words

4. The duration of fixed exchange rate regimes

5. QUEST II. A Multi-Country Business Cycle and Growth Model

6. EMU: some unanswered questions

7. The name is absent

8. Macro-regional evaluation of the Structural Funds using the HERMIN modelling framework

9. La mobilité de la main-d'œuvre en Europe : le rôle des caractéristiques individuelles et de l'hétérogénéité entre pays

10. The name is absent