William Davidson Institute Working Paper 402

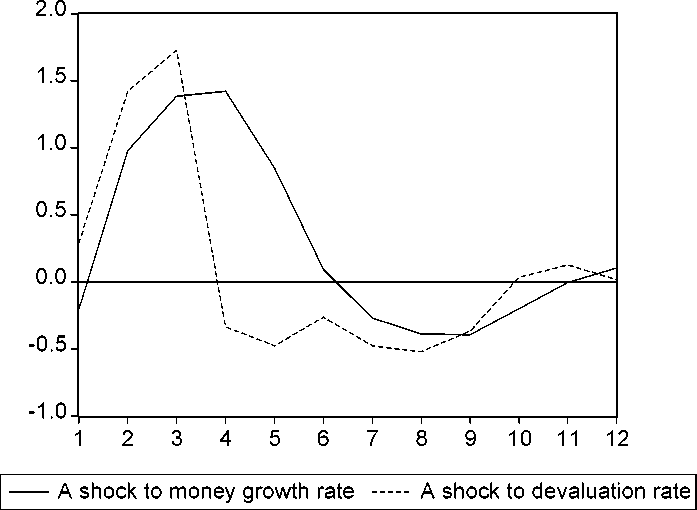

reached with a three-month lag for devaluation and a four-month lag for money. It

takes some one-year to the system to return at the pre-shock equilibrium.

Figure 10. The impulse function. Response of monthly inflation rate to one standard

deviation shock in the monthly money growth rate and in the devaluation rate. On the

horizontal axis: number of months after the shock.

This simple AR model is instructive as it points to the high speed of

transmitting nominal shocks in the Romanian economy. In mature monetary

economies, money shocks need over six months to translate into higher prices. In

Romania, the first impact can be observed only two months later.

This would point to a source of ineffectiveness of the NBR policy of managing

real exchange rates by systematic interventions in the foreign exchange market over

the 1997-2000 period. If the central bank buys dollars in an attempt to depreciate the

leu, it simultaneously increases the money stock, which, two months later, already

brings about higher inflation. In this context, the real depreciation is hard to be

achieved. The massive recourse to sterilization is the only chance to block the

increase in the money stock.

10. Conclusion and policy implications for Romania

Romania’s macroeconomic performance can be termed so far as

disappointing: the country has not been able to deliver steady growth, low

unemployment and low inflation. Many factors are microeconomic and can be related

to the slow progress with firm restructuring, privatisation and institution building. In

the text at hand we have taken these important constraints as given, to focus on the

effectiveness of monetary and exchange rate mechanisms and policies The National

Bank of Romania has been, so far, unable to carry out a consistent monetary policy,

which should subdue inflation. Under quite unfavourable circumstances and various

pressures (frequently of a political nature) it has often provided easy credit to

“sensible” sectors and dodgy commercial banks. Such quasi-fiscal operations have

been a resilient feature of NBR’s activity throughout the decade. At some moments, it

also financed directly public deficits, in contradiction with the price stability goal.

23

More intriguing information

1. Alzheimer’s Disease and Herpes Simplex Encephalitis2. Gender stereotyping and wage discrimination among Italian graduates

3. Optimal Taxation of Capital Income in Models with Endogenous Fertility

4. Mortality study of 18 000 patients treated with omeprazole

5. Improving behaviour classification consistency: a technique from biological taxonomy

6. Population ageing, taxation, pensions and health costs, CHERE Working Paper 2007/10

7. The name is absent

8. The name is absent

9. The Challenge of Urban Regeneration in Deprived European Neighbourhoods - a Partnership Approach

10. INTERPERSONAL RELATIONS AND GROUP PROCESSES