William Davidson Institute Working Paper 402

8. The exchange rate policy

Since 1997 the leu fluctuates against the major currencies in a free market

where the NBR intervenes as any other trader. However, the volume and the

frequency of the transactions of the NBR in the foreign exchange market exceed what

we normally can see as specific to a managed float regime. In mature market

economies, the central bank resorts to interventions in the foreign exchange market

only in exceptional cases, and tries to influence the exchange rate by monetary policy,

in particular by managing short-term interest rates. But given that in Romania the

Treasury bonds market is quite thin and the banking sector does not demand

refinancing credits, the central bank has limited control over market determined short-

term interest rates. So, at a first sight, it seems that if the NBR wants to alter the

international value of the leu, it can (and should) rely on direct transactions in the

foreign exchange market. Let us take a closer look to this reasoning.

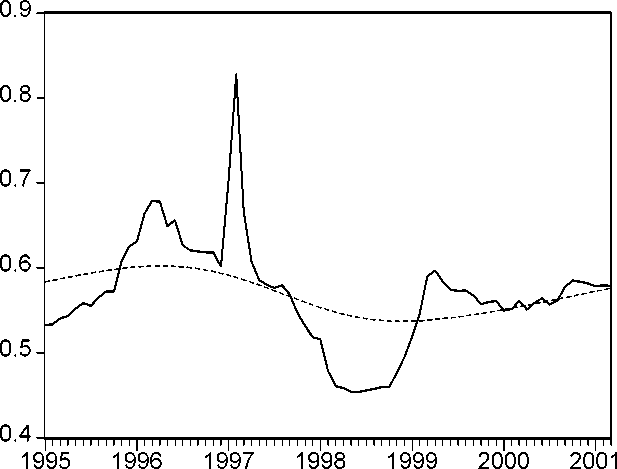

Figure 8 shows the evolution of the real exchange rate of the leu relatively to

the US dollar since 1992. During the early years of transition, there was a general

tendency of real appreciation of the leu. To a certain extent, such an evolution is

consistent with the Balassa-Samuelson paradigm19, but an excessive appreciation

would hamper export competitiveness. The structural current account deficit of

Romania throughout the last decade would point to such a weakness. Moreover, the

major difficulties faced by Romania in 1999 followed a period of sharp real

appreciation, and the recovery was accompanied by depreciation. So, what matter for

economic performance is not the dynamics of nominal, but of real exchange rates. In

low an inflation environment the difference is not so sharp; but Romania is not a low

inflation environment.

Real exchange rate ------Trend

Figure 8. Real dollar-leu exchange rate index, base 1.00 in December 1991. The trend

builds on Hodrick and Prescott filter. Price variation builds on consumer price indexes

in Romania and the US. Source: NBR and US Bureau of Labour Statistics

19 A note of caution should be kept in mind since rationing accompanied the functioning of the official

foreign exchange market until early 1997.

21

More intriguing information

1. The name is absent2. Improvement of Access to Data Sets from the Official Statistics

3. Cultural Diversity and Human Rights: a propos of a minority educational reform

4. The name is absent

5. Improving behaviour classification consistency: a technique from biological taxonomy

6. Government spending composition, technical change and wage inequality

7. The name is absent

8. Input-Output Analysis, Linear Programming and Modified Multipliers

9. Outsourcing, Complementary Innovations and Growth

10. Consumer Networks and Firm Reputation: A First Experimental Investigation