.008

Response of Y to Y

.004

.000

2 4 6 8 10 12 14 16 18 20

.008

Response to Cholesky One S.D. Innovations - 2 S.E.

Response of Y to P

.004

2 4 6 8 10 12 14 16 18 20

.008

.008

.004

.004

-.004

-.004

-.008

-.008

.8

.010

.01

2 4 6 8 10 12 14 16 18 20

2 4 6 8 10 12 14 16 18 20

-.008

Response of P to IS

.000

-.004

2 4 6 8 10 12 14 16 18 20

-.008

Response of P to M

.000

-.004

2 4 6 8 10 12 14 16 18 20

Response of M to Y

.005

.000

-.005

-.010

2 4 6 8 10 12 14 16 18 20

-.015

Response of M to P

.005

.000

-.005

-.010

-.01

2 4 6 8 10 12 14 16 18 20

Response of IS to IS

.0

2 4 6 8 10 12 14 16 18 20

.8

Response of IS to M

.4

.0

2 4 6 8 10 12 14 16 18 20

-.4

-.4

-.8

-.8

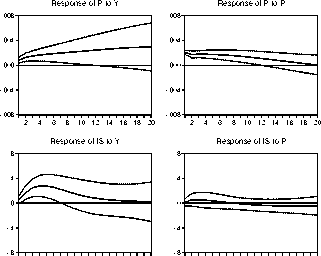

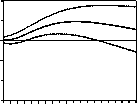

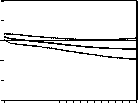

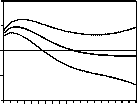

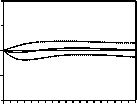

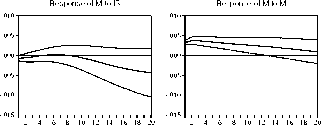

Figure 3: Impulse response analysis; basic model

the influence of money for inflation has a long-term character. In the case of the

interest rate shock, the reaction of the price level yields the ”price puzzle” which

often occurs in the VAR analysis and was also faced by RUffer and Stracca (2006) as

well as Sousa and Zaghini (2006) in the same context. The appearance of the ”price

puzzle” is sometimes thought to be caused by the lack of a variable which captures

inflation expectations (Greiber, 2007). Monetary policy makers are supposed to

raise interest rates when inflation expectations rise. When their policy cannot stop

inflation from rising, the system may identify the rise of interest rates as a trigger of

the increase in the price level. Therefore, it is recommended by Favero (2001) to use

a commodity price index that might capture inflation expectations to some degree

and may solve this problem. We considered this alternative and added a commodity

price index and the oil price as complements of our system, but, still, the ”price

17

More intriguing information

1. On the Integration of Digital Technologies into Mathematics Classrooms2. Applications of Evolutionary Economic Geography

3. Weather Forecasting for Weather Derivatives

4. The name is absent

5. NATIONAL PERSPECTIVE

6. Critical Race Theory and Education: Racism and antiracism in educational theory and praxis David Gillborn*

7. The Impact of Minimum Wages on Wage Inequality and Employment in the Formal and Informal Sector in Costa Rica

8. Momentum in Australian Stock Returns: An Update

9. BARRIERS TO EFFICIENCY AND THE PRIVATIZATION OF TOWNSHIP-VILLAGE ENTERPRISES

10. DEVELOPING COLLABORATION IN RURAL POLICY: LESSONS FROM A STATE RURAL DEVELOPMENT COUNCIL