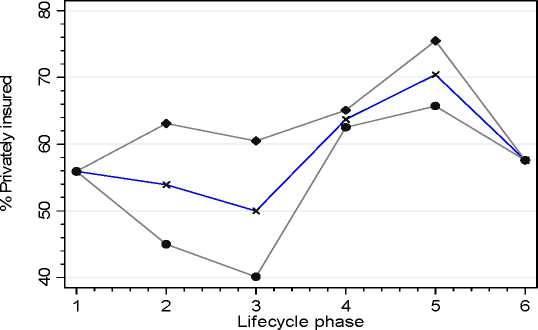

The lifecycle demand for health insurance is, in contrast to female labour supply and

household saving, complicated by the rise in health risk with age. Average female

hours are at their highest level in phase 1 of the lifecycle, however the health risk of

the household is at its lowest point in this phase, and so the demand for health

insurance is low in phase 1. In the later phases, the profiles for private health

insurance tend to converge, with both rising significantly with age, as we would

expect. Although rising health risk is obviously an important determinant of the shape

of the profiles over the lifecycle, nevertheless it is evident that households with a

higher female labour supply are more likely to purchase private insurance and to

spend more on fees.31

Figure 6a: % private health insurance

All h H1

H2

31 This is consistent with the finding of Doiron et al. (2007) that personal income effects are stronger

than other household income on the purchase of private health insurance, and that the effects of

personal income are stronger for women than for men.

18

More intriguing information

1. WP 48 - Population ageing in the Netherlands: Demographic and financial arguments for a balanced approach2. The name is absent

3. Evaluating the Impact of Health Programmes

4. TECHNOLOGY AND REGIONAL DEVELOPMENT: THE CASE OF PATENTS AND FIRM LOCATION IN THE SPANISH MEDICAL INSTRUMENTS INDUSTRY.

5. The name is absent

6. The name is absent

7. The name is absent

8. Les freins culturels à l'adoption des IFRS en Europe : une analyse du cas français

9. The name is absent

10. Structural Influences on Participation Rates: A Canada-U.S. Comparison