principal component of mortgage repayments, capital housing costs and

superannuation and life insurance. 27

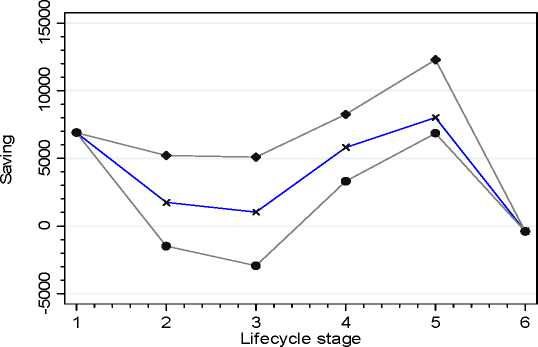

Figure 5 plots the lifecycle profiles of median saving for each household group, and

the profile for the full sample. The figure shows graphically the strong tendency for

household saving to track female labour supply. This is not a surprising, given that

the H1 household has chosen to substitute domestic for market work and therefore has

less market income available for the purpose of saving. Median household saving by

H1 households is well below that by H2 households from phase 2 to retirement. In

phase 1, median saving is high because almost all female partners work full time. In

phase 2 there is a sharp fall in the median of the full sample, due to a dramatic fall in

the saving of H1. The median saving of the H1 household is actually negative in

phases 2 and 3.

Figure 5: Lifecycle saving by household type

--All h H1

♦ H2

Again the diverse decisions of the two household groups cannot be attributed to

family size or, in this case, to the effects of family size on labour supply and therefore

on earnings, for two reasons. First, the household groups have close to the same

27 Note that total expenditure includes income tax and so saving is, in effect, computed as net income

less consumption expenditure.

16

More intriguing information

1. A Principal Components Approach to Cross-Section Dependence in Panels2. The Role of Land Retirement Programs for Management of Water Resources

3. American trade policy towards Sub Saharan Africa –- a meta analysis of AGOA

4. Optimal Private and Public Harvesting under Spatial and Temporal Interdependence

5. Impact of Ethanol Production on U.S. and Regional Gasoline Prices and On the Profitability of U.S. Oil Refinery Industry

6. PROPOSED IMMIGRATION POLICY REFORM & FARM LABOR MARKET OUTCOMES

7. Comparative study of hatching rates of African catfish (Clarias gariepinus Burchell 1822) eggs on different substrates

8. Rent Dissipation in Chartered Recreational Fishing: Inside the Black Box

9. The name is absent

10. The name is absent