COEFFICIENTS

|

Standardized |

t |

Sig. |

95% Confidence |

Correlations |

Collinearity | ||||

|

β |

Lower Bound |

Upper |

Zero-order |

Partial |

Tolerance |

VIF | |||

|

Constant |

-696.046 |

-.982 |

.328 |

-2099.02 |

706.930 | ||||

|

PHI |

0.822 |

15.769 |

.000 |

0.075 |

0.097 |

.825 |

.824 |

.994 |

1.006 |

|

EDN |

0.033 |

.640 |

.523 |

-959.697 |

1876.72 |

.095 |

.059 |

.994 |

1.006 |

a Dependent Variable: PHE

Source: Compiled from Primary Data

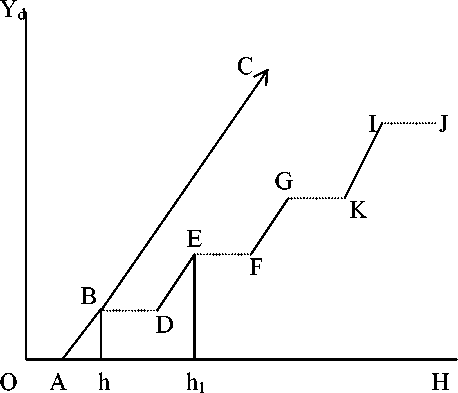

From the study it is found that as disposable

income (Yd) of the household increases,

individual takes more care of his life, hence

health expenditure (H) increases but at a

particular level of income, due to high life

risk, health expenditure becomes

independent of income and perfectly elastic,

which is termed as “High Life Risk Path

(HLRP)”. The health expenditure during

HLRP depends on household’s past saving

(S) and loanable capacity (L).

FIGURE 2

THE HEALTH EXPENDITURE CURVE

In figure 2, OA is autonomous health expenditure. In normal life, ABC is the health

expenditure curve (with linear relationship assumption between health expenditure and

disposable income) without any high life risk. But due to high life risk at Bh level of disposable

income, B is the bearable point3 and BD is the HLRP. Again normal life starts from point D to

point E. At Eh1 level of disposable income, E is the bearable point and EF is the HLRP and so

on. Hence, ABDEFGKIJ is the health expenditure path at high life risk, which is not a normal

path.

3 The bearable point is the point at which the maximum health expenditure can be financed from a particular level of

disposable income.

More intriguing information

1. TRADE NEGOTIATIONS AND THE FUTURE OF AMERICAN AGRICULTURE2. Searching Threshold Inflation for India

3. The name is absent

4. The name is absent

5. The name is absent

6. Stillbirth in a Tertiary Care Referral Hospital in North Bengal - A Review of Causes, Risk Factors and Prevention Strategies

7. Design and investigation of scalable multicast recursive protocols for wired and wireless ad hoc networks

8. AN ECONOMIC EVALUATION OF THE COLORADO RIVER BASIN SALINITY CONTROL PROGRAM

9. 5th and 8th grade pupils’ and teachers’ perceptions of the relationships between teaching methods, classroom ethos, and positive affective attitudes towards learning mathematics in Japan

10. Wirtschaftslage und Reformprozesse in Estland, Lettland, und Litauen: Bericht 2001