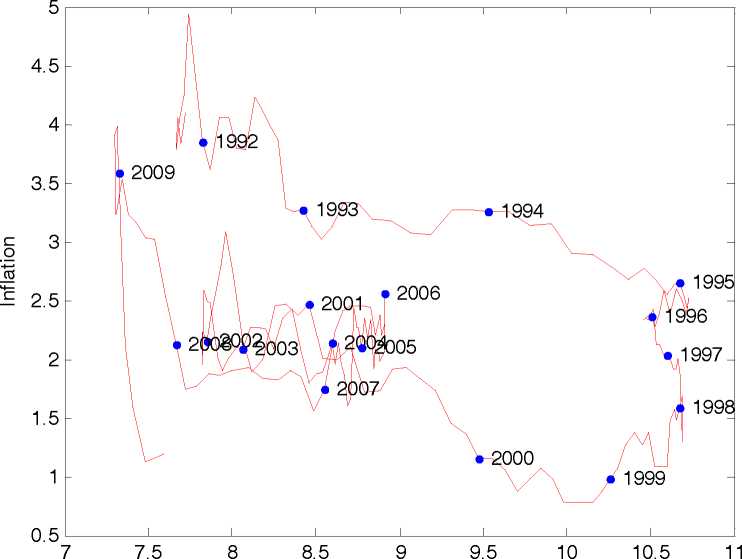

Chart 3. Inflation-unemployment cross-plot

Unemployment

3.2 Trend Inflation, Steady-State Inflation and Inflation Persistence

Our benchmark univariate model of the inflation process regresses current inflation on

a constant term and three lags of both inflation and the unemployment rate. A

Bayesian approach is taken for the estimation. We start from an appropriate but

weakly informative prior, and use the 1980s as a pre-sample to update it. We report

the results from 1990m1 onwards, therefore including the period immediately before

the Maastricht Treaty, the convergence period to meet the requirements of the Treaty,

and the first decade of EMU. After the estimation, and in order to check whether there

is time variation in the relevant parameters of the models, we perform ADF tests on

trend inflation, inflation persistence and the sum of the coefficients of unemployment.

Table 1. Tests for time variation

|

_______________________Coefficients of AR component_______________________ | |||

|

Constant |

Sum(πt-1, ∏t-2, πt-3) |

Sum(ut-1, ut-2, ut-3) | |

|

ADF test (p-value) |

-2.072 (0.256) |

-1.558 (0.503) |

-2.528 (0.110) |

|

____________________Coefficients of GARCH component____________________ | |||

|

_________________h_ |

___________________a |

__________________λ. | |

|

Parameter values |

____________0.0005 |

0.0796 |

____________0.9161 |

|

T-stats based on |

1.36 |

3.42* |

37.98** |

|

__________________Squared standardized residuals serial correlation__________________ | |||

|

___________LB(1) |

___________LB(2) |

___________LB(3) |

___________LB(4) |

|

_______________2.59 |

_______________5.69 |

_______________6.95 |

_______________7.06 |

More intriguing information

1. On the job rotation problem2. Types of Tax Concessions for Promoting Investment in Free Economic and Trade Areas

3. Testing Panel Data Regression Models with Spatial Error Correlation

4. Motivations, Values and Emotions: Three Sides of the same Coin

5. The name is absent

6. THE AUTONOMOUS SYSTEMS LABORATORY

7. Can a Robot Hear Music? Can a Robot Dance? Can a Robot Tell What it Knows or Intends to Do? Can it Feel Pride or Shame in Company?

8. Secondary school teachers’ attitudes towards and beliefs about ability grouping

9. On the Relation between Robust and Bayesian Decision Making

10. The name is absent