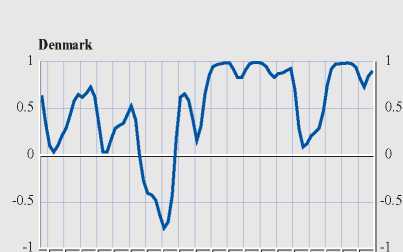

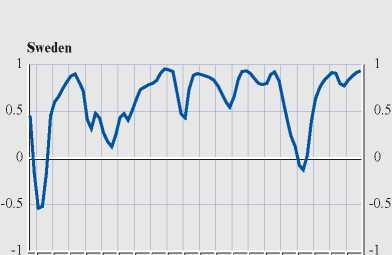

Chart 10 Business cycle synchronisation

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

Sources: Eurostat, NCBs, ECB calculations.

Note : Business cycle correlation is measured by the correlation coefficient of an 11 -quarter rolling window between the business cycle

component of each individual country and the (available) business cycle component for the rest of the EU countries (applying country weights

to each individual EU country business cycle component).

3.3.1 AGGREGATE VERSUS SECTORAL BUSINESS

CYCLE SYNCHRONISATION

Measuring business cycle correlations for each

available country against the average cycle of

the remaining EU countries, Chart 10 gives an

overview of the evolution of business cycle

synchronisation.

The Chart confirms earlier analyses in this area

showing that business cycle synchronisation

increased at the beginning of the 1990s and

continued throughout the decade, despite a

short period of relatively lower synchronisation

in the aftermath of the Asian and Russian crises

(1997 and 1998) that affected Germany

relatively more strongly than the other EU

countries.51 This de-synchronisation was

particularly important for some smaller EU

countries (Denmark, Sweden), where even

some divergence was observed in 1997, but also

for countries like France and Italy, albeit on a

smaller scale.

Similarly to the aggregate business cycle,

synchronisation can also be measured on the

sectoral level, as presented in Table 10. In this

table, correlation coefficients for each sector

between individual countries and the EU

countries average are presented:

51 This also holds true for those EU countries for which the analysis

could not be carried out on account of missing data. Looking at

annual data over a longer period, Belo (2001) detects cyclical

convergence for Ireland, Portugal and Greece over the period

1960-1999 yielding qualitatively speaking the same conclusions

as in this report; F. Belo (2001), “Some facts about the cyclical

convergence in the euro zone”, Banco de Portugal Working

Paper, 7-01.

44

ECB

Occasional Paper No. 19

July 2004

More intriguing information

1. The name is absent2. Convergence in TFP among Italian Regions - Panel Unit Roots with Heterogeneity and Cross Sectional Dependence

3. Firm Creation, Firm Evolution and Clusters in Chile’s Dynamic Wine Sector: Evidence from the Colchagua and Casablanca Regions

4. Cyber-pharmacies and emerging concerns on marketing drugs Online

5. Migration and Technological Change in Rural Households: Complements or Substitutes?

6. The name is absent

7. Testing the Information Matrix Equality with Robust Estimators

8. The name is absent

9. The name is absent

10. Chebyshev polynomial approximation to approximate partial differential equations