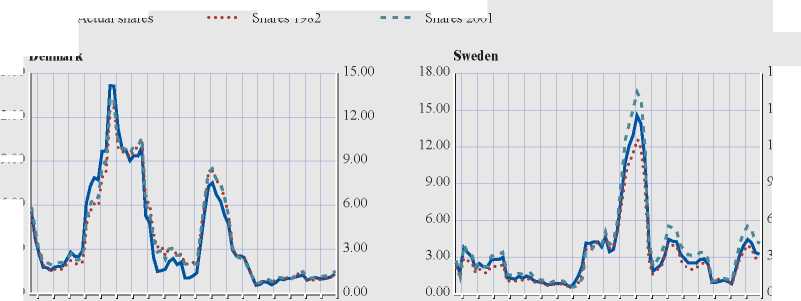

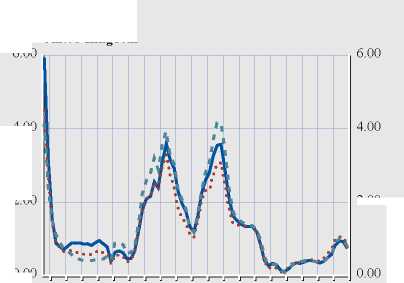

Chart 9 Sectoral shifts and volatility (cont’d)

Actual shares

12.00

Shares 1982

Shares 2001

Denmark

15.00

18.00

15.00

12.00

9.00

6.00

6.00

3.00

3.00

0.00

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

0.00

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

9.00

United Kingdom

6.00

0.00

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

4.00

2.00

2.00

The figure reports the variance of the aggregate business

cycle component at the actual sectoral specialisation for

each individual observation (solid line) and the variance

of the aggregate business cycle component where the

sectoral specialisation has been fixed at its initial value

(dashed line).

Sources : Eurostat, NCBs, ECB calculations.

Note: See Annex 4.2.2.2 for a discussion of the underlying methodology and a presentation of volatility developments using the same scale for

all countries.

almost consistently lower over the period after

1991 following the increased weight of low-

volatility business sector services. Finally,

Sweden seems to have experienced a slight

increase of its aggregate volatility, mainly on

account of a slightly increasing share of

industry in its final output.

3.3 BUSINESS CYCLE SYNCHRONISATION

ACROSS EU COUNTRIES: SECTORAL

ORIGINS

Business cycle synchronisation relates to the

degree of co-movement of aggregate production

across a group of countries. Analysing the

synchronisation of business cycles at the

sectoral level is relevant in this respect, given

that changes in the composition of output could

have impacted upon business cycle

synchronisation. Nevertheless, additional

factors may offset the negative impact of

sectoral specialisation on the harmonisation of

business cycles, as will be discussed in the next

section.50

50 It is, however, not clear how precisely convergence between

business cycles should be assessed. Different suggestions have

been put forward, including increased bivariate correlations,

decreased cyclical disparity or emerging common factors that

drive individual countries’ business cycles. Using the business

cycle components presented in the preceding section, bivariate

correlations have been preferred here. For an overview of

measures of business cycle synchronisation, see M. Massmann

and J. Mitchell (2002), “Have UK and euro zone business cycles

become more correlated?”, National Institute Economic

Review, 182. For a recent analysis of the factors driving business

cycle synchronisation in G7 countries, see A. Monfort, J.-P.

Renne, R. Rüffer and G. Vitale (2003), “Is economic activity in

the G7 synchronised? Common shocks versus spillover effects”,

CEPR Discussion Paper, 4119.

42

ECB

Occasional Paper No. 19

July 2004

More intriguing information

1. The name is absent2. Strategic Policy Options to Improve Irrigation Water Allocation Efficiency: Analysis on Egypt and Morocco

3. Parent child interaction in Nigerian families: conversation analysis, context and culture

4. Evidence on the Determinants of Foreign Direct Investment: The Case of Three European Regions

5. Tobacco and Alcohol: Complements or Substitutes? - A Statistical Guinea Pig Approach

6. The Mathematical Components of Engineering

7. The name is absent

8. The name is absent

9. CAN CREDIT DEFAULT SWAPS PREDICT FINANCIAL CRISES? EMPIRICAL STUDY ON EMERGING MARKETS

10. Biological Control of Giant Reed (Arundo donax): Economic Aspects