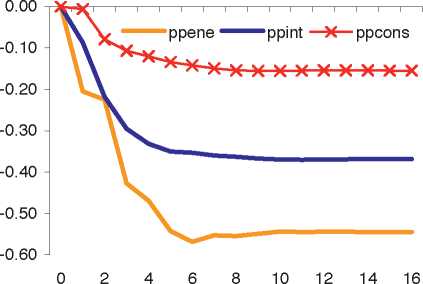

of about -0.47% after 4 quarters. It gets progressively weaker following the pricing chain on

the PPI, with an effect of -0.35% after 5 quarters on PPI intermediate goods, and of -0.15%

after about 8 quarters for PPI consumer goods.

Chart 5 Impact multiplier of the exchange rate

(deviation from baseline following 1% increase in nominal effective exchange rate)

Effect of 1% NEER appreciation on

producer prices

(deviation from baseline)

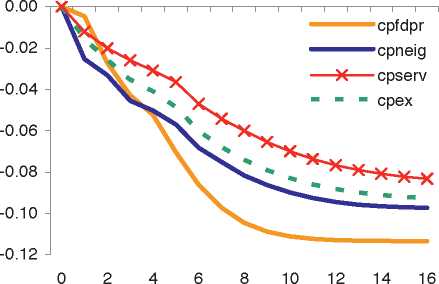

Effect of 1% NEER appreciation on

consumer prices

(deviation from baseline)

PPENE: PPI energy; PPINT: PPI intermediate goods; PPCONS: PPI consumer goods; CPFDPR: HICP

processed food; CPNEIG: HICP non-energy industrial goods; CPSERV: HICP services, CPEX: HICP excluding

unprocessed food and energy.

The timing and the pass-through to the energy and consumer goods’ PPI is similar to Hahn

(2007) who found an impact of -0.68 and -0.16 after 8 quarters for these two sectors,

respectively, while the effect on PPI intermediate goods is somewhat lower according to her

results (-0.17 after 8 quarters). The results of Bailliu and Fujii (2004) are, with a long-run

impact of -0.28 to -0.37 on total producer prices, also in line with our results, while Campa

and Gonzalez Minguez (2006), Faruqee (2006) and Hahn (2003) point to somewhat lower

effects on total euro area producer prices (-0.12, -0.17 and -0.06, respectively). Note that the

latter four studies also include capital goods in the aggregate which is not taken into account

in our study. According to Hahn (2007), the exchange rate pass-through to capital goods

consumer prices is around -0.04, i.e. much smaller than what has been found for the other

sectors. Choudri et al. (2002) estimated a VAR for the G7 countries excluding the US and

found an exchange rate pass-through of -0.15 on producer prices after 10 quarters.

For consumer prices, the effect is rather similar for processed food and non-energy industrial

goods prices with an effect around -0.10% after 16 quarters, and a bit smaller for services

prices (around -0.08%). The somewhat weaker effect on services prices reflects the lower

import content of this component, along with the higher labour intensity of this sector. The

ECB ■

Working Paper Series No 1104

November 2009∣ 15

More intriguing information

1. Private tutoring at transition points in the English education system: its nature, extent and purpose2. The name is absent

3. The name is absent

4. A Rational Analysis of Alternating Search and Reflection Strategies in Problem Solving

5. Climate change, mitigation and adaptation: the case of the Murray–Darling Basin in Australia

6. The name is absent

7. QUEST II. A Multi-Country Business Cycle and Growth Model

8. Linking Indigenous Social Capital to a Global Economy

9. WP 1 - The first part-time economy in the world. Does it work?

10. Making International Human Rights Protection More Effective: A Rational-Choice Approach to the Effectiveness of Ius Standi Provisions