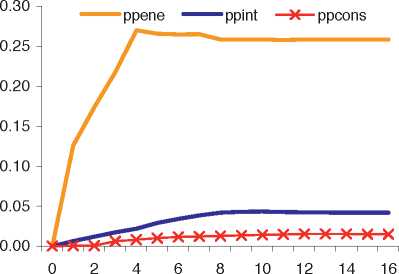

Regarding the impact of a 1% increase in energy commodity prices (see Chart 6), except for

the direct effect on PPI energy, the effect is rather muted. According to the result, the impact

amounts to an increase by 0.27% on PPI energy after 4 quarters, by 0.022% in PPI

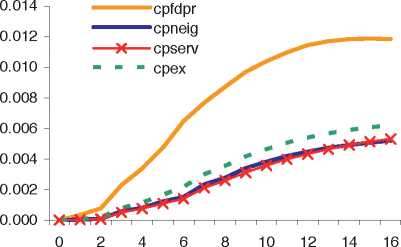

intermediate and 0.008% in PPI consumer goods. Regarding the impact on consumer prices,

the impact is rather similar for non-energy industrial goods and services prices (around

0.005% after 16 quarters), while it is stronger for processed food prices (about 0.012%) , with

an overall slower pass-through compared to producer prices. Using the weighted average for

the CPEX suggests an impact of 0.006%. It should be noted that the present study only looks

into the indirect effect on the non-volatile components of the HICP, while the direct effect on

the HICP energy would be significantly stronger and more immediate. A rule of thumb would

suggest that a 1% increase in oil prices would lead to a 0.01-0.02% increase in total HICP due

to the direct effect of oil prices.11 A somewhat astonishing fact is that the effect on processed

food prices is about twice as large as that on the other consumer prices which is due to a

stronger impact of PPI energy and intermediate goods on this component of the HICP. This

may reflect the relatively high energy content in food production.

Chart 6 Impact multiplier of energy commodity prices

(deviation from baseline following 1% increase in energy commodity prices)

Effect of 1% increase in energy

commodity prices on producer prices

(deviation from baseline)

Effect of 1% increase in energy

commodity prices on consumer prices

(deviation from baseline)

PPENE: PPI energy; PPINT: PPI intermediate goods; PPCONS: PPI consumer goods; CPFDPR: HICP

processed food; CPNEIG: HICP non-energy industrial goods; CPSERV: HICP services, CPEX: HICP excluding

unprocessed food and energy.

The impact on consumer prices according to our models is roughly in line with that of

different macro-models when taking into account the fact that we only consider the HICP

excluding unprocessed food and energy here. In particular, the ECB AWM, the EC QUEST,

11 See European Central Bank (2004).

И ECB

Working Paper Series No 1104

November 2009

More intriguing information

1. The name is absent2. APPLYING BIOSOLIDS: ISSUES FOR VIRGINIA AGRICULTURE

3. Spousal Labor Market Effects from Government Health Insurance: Evidence from a Veterans Affairs Expansion

4. Fiscal Sustainability Across Government Tiers

5. SLA RESEARCH ON SELF-DIRECTION: THEORETICAL AND PRACTICAL ISSUES

6. The name is absent

7. The name is absent

8. The Effects of Reforming the Chinese Dual-Track Price System

9. Do Decision Makers' Debt-risk Attitudes Affect the Agency Costs of Debt?

10. On the Desirability of Taxing Charitable Contributions