the NiGEM and the OECD Interlink predict a first year impact of a 50% increase in oil prices

on consumer prices of 0.3% to 0.6%, and a cumulated 0.5% to 1.0% impact over 3 years.12

This is significantly higher than the 0.3% we would get for a 50% increase in energy prices

on the HICP excluding unprocessed food and energy after 4 years, but roughly in line with

our results when allowing for an additional 0.5%-1.0% due to the direct effect of energy on

the overall HICP. Looking at the results from small-scale models, Hahn (2003) suggests that a

50% increase in oil prices leads to a 0.9% increase in overall consumer prices after 1 year,

1.6% after 2 years and 2.2% after 3 years, somewhat higher than the results above.

A specificity of our approach is that, unlike other models, we estimate the impact of energy

and non-energy commodities separately and we further split the latter into food and industrial

raw material prices. This is particularly important in our pricing chain analysis, as different

commodity prices might have a different impact on the individual price components.

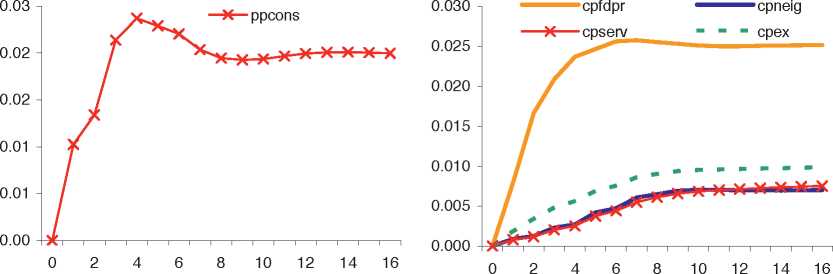

The results for food commodity prices are shown in Chart 7. The effect is the strongest for

PPI consumer goods (around 0.02% after 16 quarters, with most of the impact coming

through within the first year), while food commodity prices have, unsurprisingly, not been

found to be significant for the other two PPI components.

Chart 7 Impact multiplier of food commodity prices

(deviation from baseline following 1% increase in food commodity prices)

Effect of 1% increase in food comm.

prices on producer prices

(deviation from baseline)

Effect of 1% increase in food comm.

prices on consumer prices

(deviation from baseline)

PPENE: PPI energy; PPINT: PPI intermediate goods; PPCONS: PPI consumer goods; CPFDPR: HICP

processed food; CPNEIG: HICP non-energy industrial goods; CPSERV: HICP services, CPEX: HICP excluding

unprocessed food and energy.

12 See European Central Bank (2004).

ECB ■

Working Paper Series No 1104

November 2009∣ 19

More intriguing information

1. On the Existence of the Moments of the Asymptotic Trace Statistic2. Feature type effects in semantic memory: An event related potentials study

3. The Impact of Financial Openness on Economic Integration: Evidence from the Europe and the Cis

4. The name is absent

5. Proceedings of the Fourth International Workshop on Epigenetic Robotics

6. Should Local Public Employment Services be Merged with the Local Social Benefit Administrations?

7. Gerontocracy in Motion? – European Cross-Country Evidence on the Labor Market Consequences of Population Ageing

8. Creating a 2000 IES-LFS Database in Stata

9. ENERGY-RELATED INPUT DEMAND BY CROP PRODUCERS

10. How we might be able to understand the brain