Figure 5.3 (continued)

Portugal

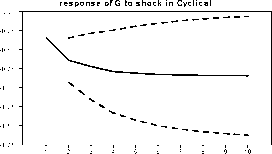

response of G to shock in Cyclical

1 2 3 4 5 6 7 8 9 10

response of T to shock in Cyclical

1.40

1.20 -

1.00 -

0.80 -

0.60 -

0.40 -

0.20

1 2 3 4 5 6 7 8 9 10

Spain

response of Y to shock in Supply

6.40

4.80

3.20

1.60

0.00

-1.60

123456789 10

response of Y to shock in Cyclical

1.00

0.75

0.50

0.25

0.00

-0.25

-0.50

-0.75

-1.00

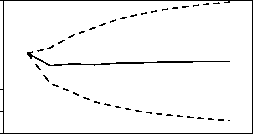

response of G to shock in Supply

-1.00

-2.00

-3.00

-4.00

-5.00

-6.00

-7.00

123456789 10

1 23456789 10

response of T to shock in Supply

2.00

1.00

0.00

-1.00

-2.00

-3.00

-4.00

123456789 10

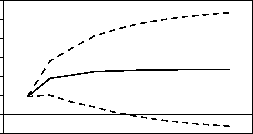

response of T to shock in Fiscal

9.60

8.00

6.40

4.80

3.20

1.60

0.00

-1.60

1 23456789 10

0.00

-2.00

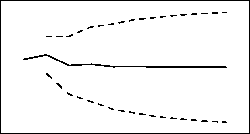

response of T to shock in Cyclical

-0.50

-1.00

-1.50

1 23456789 10

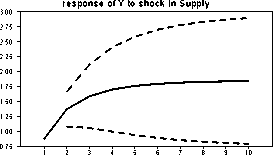

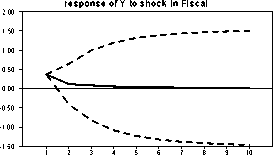

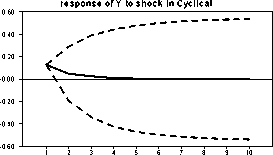

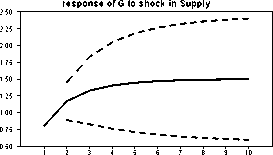

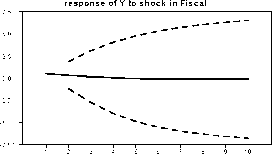

The fiscal shock then regards all discretionary policy interventions on spending and/or

revenues that are not systematically related to the cycle and have only temporary effects

on the economy. These discretionary fiscal shocks have somewhat prolonged effects on

output. There is a lot of uncertainty around this effect and none of the responses is really

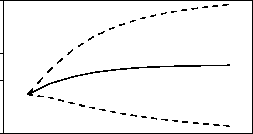

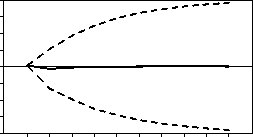

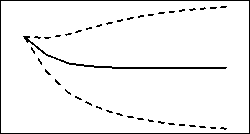

significant. We scale the impulse responses in Figure 5.3 such that they always display

138

More intriguing information

1. IMPLICATIONS OF CHANGING AID PROGRAMS TO U.S. AGRICULTURE2. Developments and Development Directions of Electronic Trade Platforms in US and European Agri-Food Markets: Impact on Sector Organization

3. The name is absent

4. A Consistent Nonparametric Test for Causality in Quantile

5. Emissions Trading, Electricity Industry Restructuring and Investment in Pollution Abatement

6. Running head: CHILDREN'S ATTRIBUTIONS OF BELIEFS

7. On Dictatorship, Economic Development and Stability

8. Corporate Taxation and Multinational Activity

9. The name is absent

10. What Drives the Productive Efficiency of a Firm?: The Importance of Industry, Location, R&D, and Size