Source: Velfærdskommissionen (2005d)

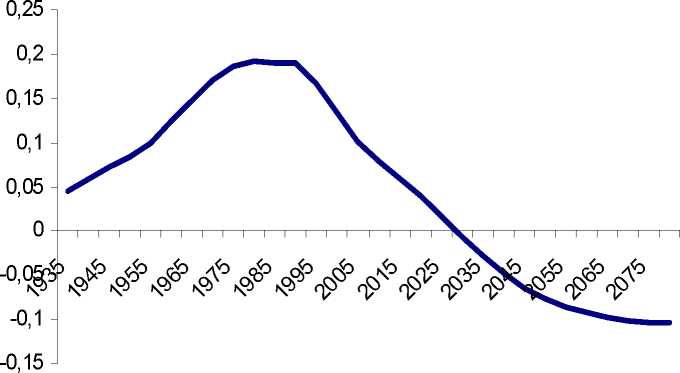

Although the prefunding strategy smoothens taxes over time, it also implies

a generational profile for the tax burden. This is so since the tax payments

for a long period of time (before 2080) would be larger under the prefunding

strategy compared to the PAYG-strategy. Considering the taxes paid by a given

generation it follows that all generations born before 2030 will have to face a

larger tax payment compared to PAYG-financing, and vice versa for generations

born after 2030, cf figure 818.

The choice of strategy has the largest implications for generations born be-

tween 1970 and 2000. For these generations the present value of the difference

corresponds to 0.2 million Dkr per person over lifetime. The gain to generations

born after 2060 under the prefunding strategy has a present value of about 0.1

million Dkr per person evaluated over life time.

Figure 8: Difference in net-payments across

generations: Sustainable vs PAYG tax

Note: Present value of the difference in tax payments depending on the year of

birth, million Dkr per person

Source: Velfærdskommissionen (2005d)

The distribution of gains and losses in net-contributions to the public sec-

tor can approximately be used to assess the relative change in utility for each

generation. This is so since the effects on wages and prices of the two financing

strategies are fairly similar compared to the differences in tax payments. Ba-

sically, the prefunding strategy implies that current generations are worse off

18This calculation is based on an earlier analysis, Velfærdskommissionen (2004). There is,

however, no qualitaty difference between the two.

19

More intriguing information

1. The growing importance of risk in financial regulation2. Industrial districts, innovation and I-district effect: territory or industrial specialization?

3. DISCUSSION: POLICY CONSIDERATIONS OF EMERGING INFORMATION TECHNOLOGIES

4. Sex differences in the structure and stability of children’s playground social networks and their overlap with friendship relations

5. The name is absent

6. Naïve Bayes vs. Decision Trees vs. Neural Networks in the Classification of Training Web Pages

7. Spousal Labor Market Effects from Government Health Insurance: Evidence from a Veterans Affairs Expansion

8. ‘I’m so much more myself now, coming back to work’ - working class mothers, paid work and childcare.

9. Flatliners: Ideology and Rational Learning in the Diffusion of the Flat Tax

10. FUTURE TRADE RESEARCH AREAS THAT MATTER TO DEVELOPING COUNTRY POLICYMAKERS