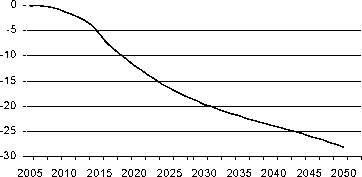

interest rates by about 60 BP in the long run and lead to an increase in the capital stock of about

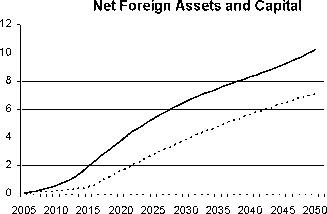

7%. Notice, however, a significant part of the additional savings would flow abroad. Foreign

wealth as a per cent of GDP would increase by about 10% points, while domestic capital as a per

cent of GDP would only increase by 7% points. Associated with the reform is a redistribution of

financial wealth from pensioners to worker households. These results compare to a reduction of

the real interest rate of 275 BP in the closed economy model of Gertler, accompanied by an

increase in the capital stock of 20%.

Real Interest Rate

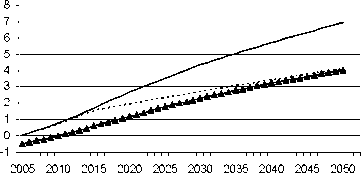

Figure 2: Reducing PAYG Pensions (2.5% of GDP)

GDP, Consumption, Capital

I Capital c Consumption .......GDP ∣

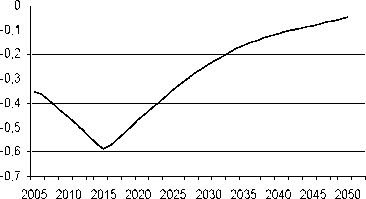

Consumption to GDP ratio

Capital to GDP ratio------Net foreign assets

One striking feature of this comparison is the relatively small crowding out effect of both

government debt and the PAYG social security system. Two features of the model are probably

crucial for this result. First unlike Gertler who models the US as a closed economy, we model the

EU economy as having access to international capital markets. Second, we assume a higher

intertemporal elasticity of substitution (σ), namely .5 vs. .25 in Gertler’s paper. Both features tend

to reduce the crowding out effect. The openness assumption implies that interest rates are

essentially determined by world savings and investment. A higher σ induces a stronger response

of savings to the initial wealth shock and does therefore require a smaller long run interest rate

response.

82

More intriguing information

1. Unilateral Actions the Case of International Environmental Problems2. WP RR 17 - Industrial relations in the transport sector in the Netherlands

3. Crime as a Social Cost of Poverty and Inequality: A Review Focusing on Developing Countries

4. Pursuit of Competitive Advantages for Entrepreneurship: Development of Enterprise as a Learning Organization. International and Russian Experience

5. Achieving the MDGs – A Note

6. The open method of co-ordination: Some remarks regarding old-age security within an enlarged European Union

7. DETERMINANTS OF FOOD AWAY FROM HOME AMONG AFRICAN-AMERICANS

8. The name is absent

9. The name is absent

10. Better policy analysis with better data. Constructing a Social Accounting Matrix from the European System of National Accounts.