Table 2:

Baseline Scenario: Keeping Generosity of PAYG

|

2004 |

2010 |

2020 |

2030 |

2040 |

2050 | |

|

GDP per capita |

1.7 |

1.7 |

1.6 |

1.5 |

1.3 |

1.2 |

|

Private Investment/GDP |

15.5 |

16.5 |

18.1 |

19.3 |

19.3 |

19.0 |

|

Unemployment Rate |

8.1 |

8.3 |

9.0 |

10.0 |

11.3 |

12.8 |

|

Real Interest Rate |

4.9 |

4.6 |

4.0 |

3.4 |

3.0 |

2.9 |

|

Retiree Cons ./Worker Cons. |

1.8 |

1.7 |

1.7 |

1.6 |

1.6 |

1.6 |

|

Pension/GDP |

9.7 |

10.3 |

11.6 |

13.3 |

15.4 |

17.3 |

|

Social Security Contributions |

14.9 |

15.8 |

17.8 |

20.4 |

23.5 |

26.5 |

GDP per capita: % deviation from baseline levels. The remaining figures are percentage point deviations

from baseline levels.

4.2. Scenario 1: Debt financing of additional pension spending after 2005

The government guarantees the 2005 pension replacement rate and at the same time freezes the

pension contribution to the current level. The difference between contributions and actual pension

expenditure is financed via an increase in government debt. With a constant contribution rate (of

currently 16%) the share of pensions covered by the PAYG contribution would decline from 100%

to about 66% in 2050. In other words the pension contributions of workers would only finance a

replacement rate of about 50% in 2050. After 2050 debt accumulation is stopped via an increase in

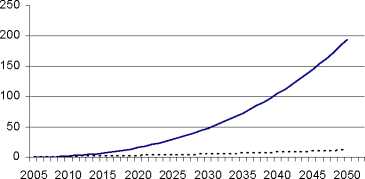

lump sum taxes. As shown in figure 3, debt is on an explosive and clearly unsustainable path.

Debt and Deficit to GDP Ratio

------Debt to GDP ratio .......Deficit to GDP ratio

Figure 3 Debt Financing of additional Pensions

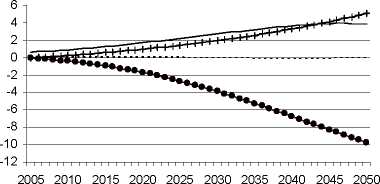

Employment, GDP, Consumption and Capital

—I—Employment .......GDP -----Consumption ∙ Capitall

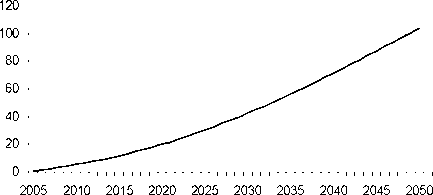

Real Interest Rate

84

More intriguing information

1. Personal Experience: A Most Vicious and Limited Circle!? On the Role of Entrepreneurial Experience for Firm Survival2. The name is absent

3. Informal Labour and Credit Markets: A Survey.

4. The name is absent

5. Innovation in commercialization of pelagic fish: the example of "Srdela Snack" Franchise

6. The name is absent

7. Education Research Gender, Education and Development - A Partially Annotated and Selective Bibliography

8. The name is absent

9. Word Sense Disambiguation by Web Mining for Word Co-occurrence Probabilities

10. he Virtual Playground: an Educational Virtual Reality Environment for Evaluating Interactivity and Conceptual Learning