1.3 Definitions and basic characteristics

Dependence on beta

Gaussian, Cauchy, and Levy distributions

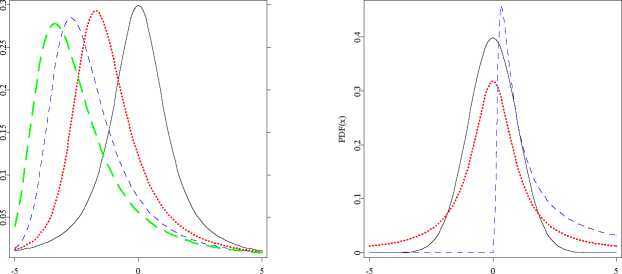

Figure 1.2: Left panel: Stable pdfs for α = 1.2 and β = 0 (black solid line), 0.5

(red dotted line), 0.8 (blue dashed line) and 1 (green long-dashed

line). Right panel : Closed form formulas for densities are known

only for three distributions - Gaussian (α = 2; black solid line),

Cauchy (α = 1; red dotted line) and Levy (α = 0.5, β = 1; blue

dashed line). The latter is a totally skewed distribution, i.e. its

support is R+. In general, for α < 1 and β = 1 (-1) the distribution

is totally skewed to the right (left).

θ STFstab02.xpl

The S,°, (σ,β,μ0) parameterization is a variant of Zolotariev’s (M)-parameteri-

zation (Zolotarev, 1986), with the characteristic function and hence the density

and the distribution function jointly continuous in all four parameters, see the

right panel in Figure 1.3. In particular, percentiles and convergence to the

power-law tail vary in a continuous way as α and β vary. The location parame-

ters of the two representations are related by μ = μ0 — βσ tan πα for α = 1 and

μ = μ0 — βσ - ln σ for α = 1. Note also, that the traditional scale parameter

σG of the Gaussian distribution defined by:

fG (x ) = v2n^rG exp ½—— ¾, (1.4)

is not the same as σ in formulas (1.2) or (1.3). Namely, σG = -√z2σ.

More intriguing information

1. Visual Artists Between Cultural Demand and Economic Subsistence. Empirical Findings From Berlin.2. A THEORETICAL FRAMEWORK FOR EVALUATING SOCIAL WELFARE EFFECTS OF NEW AGRICULTURAL TECHNOLOGY

3. Gender and headship in the twenty-first century

4. The name is absent

5. Trade and Empire, 1700-1870

6. The Impact of EU Accession in Romania: An Analysis of Regional Development Policy Effects by a Multiregional I-O Model

7. The technological mediation of mathematics and its learning

8. The name is absent

9. The name is absent

10. Ability grouping in the secondary school: attitudes of teachers of practically based subjects