J.Q. Smith and Antonio Santos

ple, in the second sub-sample we compared the density f (α852∖y 1,... ,y852,θ) with

f (α852∖y 1,... ,y1000,θ), which we might have expected to be close. The difference

between the filter distribution obtained using the first order particle filter was enor-

mous in comparison with the smoothing distribution. The same did not occur with

the second order particle filter, which is a clear indication of the feasibility of the

procedures presented in this paper.

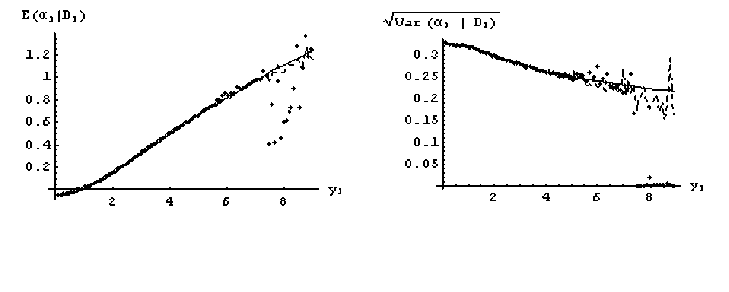

Figure 4: Comparison of particle filter procedures using the first and second order ap-

proximation to the log-likelihood function in a SV model. Left: mean evolution; Right:

standard deviation evolution; exact path (solid line); first order (dotted line); second order

(dashed line).

To better understand the infeasibility of using the first order APF to forecast the

variance evolution associated with stock returns within a standard SV model, we

present here a simple simulation that highlights the problems associated with the

existence of outliers. We illustrate these problems applied to update the distribution

of the first state, α1 , in a standard SV model. It is supposed that α0 follows a

Gaussian distribution with mean m0 and variance C0 . In the univariate model, the

updated distribution of α1∖D1, up to a normalizing constant c, has a known form

G.E.M.F - F.E.U.C.

18

More intriguing information

1. Cyclical Changes in Short-Run Earnings Mobility in Canada, 1982-19962. A Note on Costly Sequential Search and Oligopoly Pricing (new title: Truly Costly Sequential Search and Oligopolistic Pricing,)

3. THE USE OF EXTRANEOUS INFORMATION IN THE DEVELOPMENT OF A POLICY SIMULATION MODEL

4. Agricultural Policy as a Social Engineering Tool

5. AGRIBUSINESS EXECUTIVE EDUCATION AND KNOWLEDGE EXCHANGE: NEW MECHANISMS OF KNOWLEDGE MANAGEMENT INVOLVING THE UNIVERSITY, PRIVATE FIRM STAKEHOLDERS AND PUBLIC SECTOR

6. Crime as a Social Cost of Poverty and Inequality: A Review Focusing on Developing Countries

7. The name is absent

8. Feeling Good about Giving: The Benefits (and Costs) of Self-Interested Charitable Behavior

9. APPLYING BIOSOLIDS: ISSUES FOR VIRGINIA AGRICULTURE

10. The name is absent