J.Q. Smith and Antonio Santos

the particle filter procedure from the first period in all three sub-samples to both

algorithms and analysed the posterior distribution of each. A comparison was then

made between these distributions and the respective smoothing distribution.

In general, rudimentarily applied particle filter procedures have certain difficul-

ties in dealing with extreme observations. We therefore focused our attention on the

distributions of the states associated with extreme observations. Pitt and Shephard

(1999) applied the APF based on a first order approximation to the log-likelihood

function to some less challenging financial time series such as that representing the

evolution of the exchange rate of the Pound against the Dollar. However, stock

return series typically exhibit more extreme observations, so even the APF based

on a first order approximation to the log-likelihood starts to breakdown.

0 500 1000 1500

5

4

3

2

1

0 200 400 600 800 1000

6

0 200 400 600 800 1000

4

2

0

6

4

2

0

0 500 1000 1500

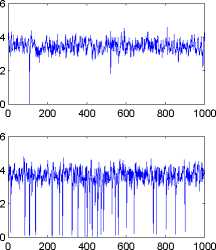

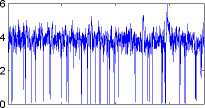

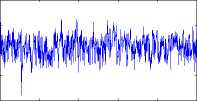

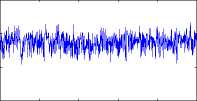

Figure 2: Difference between maximum and minimum value particles. Left-hand side:first

order filter;Right-hand side:second order filter. Each row corresponds to a different sub-

sample.

It can be seen that sample impoverishment for the APF, based on a first order

approximation particle filter applied to the series presented here, is sometimes ex-

G.E.M.F - F.E.U.C.

16

More intriguing information

1. A Rational Analysis of Alternating Search and Reflection Strategies in Problem Solving2. Computational Batik Motif Generation Innovation of Traditi onal Heritage by Fracta l Computation

3. Governance Control Mechanisms in Portuguese Agricultural Credit Cooperatives

4. Agricultural Policy as a Social Engineering Tool

5. Stakeholder Activism, Managerial Entrenchment, and the Congruence of Interests between Shareholders and Stakeholders

6. The name is absent

7. Knowledge and Learning in Complex Urban Renewal Projects; Towards a Process Design

8. ALTERNATIVE TRADE POLICIES

9. The name is absent

10. The name is absent