J.Q. Smith and Antonio Santos

6 An empirical demonstration

In this section we intend to demonstrate empirically that the first order APF ap-

proximation is not reliable when applied to a stock return series, namely, when it has

to update the distribution of the states associated with extreme observations. We

use a series of graphs displays and tables of results that try to illustrate that, with

the first order approximation, there are situations where sample impoverishment is

extreme.

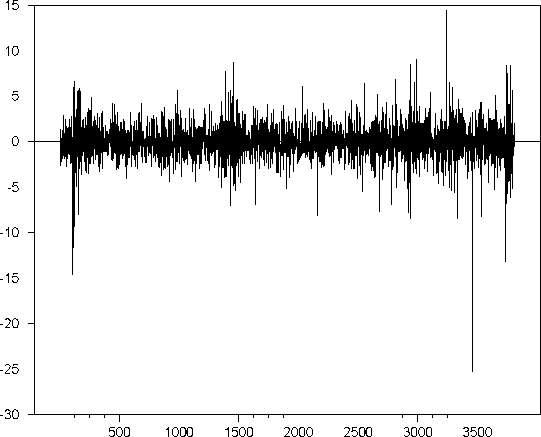

Figure 1: Rolls Royce stock returns

We analysed a series of daily returns regarding the Rolls Royce stock, traded on

the London Stock Exchange. In this series we had 3818 observations. This series is

depicted in Figure 1 and shows all the main characteristics found in the majority

of financial time series, e.g., the presence of extreme observations and volatility

clustering. We considered three sub-samples and analysed each one by adjusting an

SV model to fit the data (Table 1). The parameters were estimated as being the

G.E.M.F - F.E.U.C.

14

More intriguing information

1. The name is absent2. Consciousness, cognition, and the hierarchy of context: extending the global neuronal workspace model

3. Ruptures in the probability scale. Calculation of ruptures’ values

4. BILL 187 - THE AGRICULTURAL EMPLOYEES PROTECTION ACT: A SPECIAL REPORT

5. Thresholds for Employment and Unemployment - a Spatial Analysis of German Regional Labour Markets 1992-2000

6. The name is absent

7. AN EXPLORATION OF THE NEED FOR AND COST OF SELECTED TRADE FACILITATION MEASURES IN ASIA AND THE PACIFIC IN THE CONTEXT OF THE WTO NEGOTIATIONS

8. Asymmetric transfer of the dynamic motion aftereffect between first- and second-order cues and among different second-order cues

9. Fiscal Insurance and Debt Management in OECD Economies

10. The name is absent