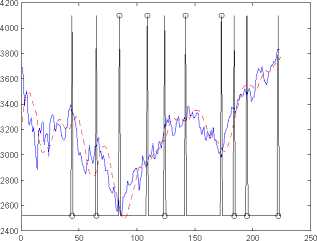

(a) Underlying (—), trend (--), prediction of abrupt (b) Risk-free ∆ tracking (—) and ∆ tracking (- -),

change locations (l) and their directions (o) prediction of abrupt change locations (l)

inria-00457222, version 1 - 16 Feb 2010

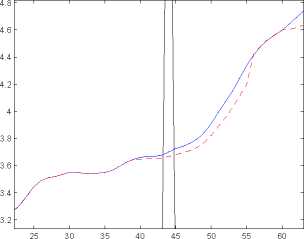

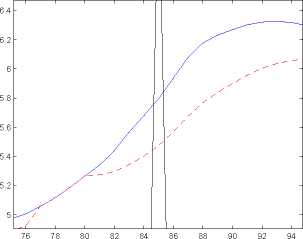

(c) Zoom on (b) (d) Zoom on (b)

Figure 4: Example 1 (continued): CFU9PY3500

[14] Fliess M., Join C., Sira-Ramirez H., Non-linear estimation is

easy, Int. J. Model. Identif. Control, 4, 12-27, 2008 (available at

http://hal.inria.fr/inria-00158855/en/).

[15] Garcia Coiiado F.A., d’Andrea-Novei B., Fliess M., Mounier

H., Analyse frequentielle des derivateurs algébriques, XXIIe Coll. GRETSI,

Dijon, 2009 (available at http://hal.inria.fr/inria-00394972/en/).

[16] Haug E.G., Derivatives: Models on Models, Wiley, 2007.

[17] Haug E.G., Taieb N.N., Why we have never used the Black-Scholes-

Merton option pricing formula, Working paper (5th version), 2009 (available

at http://ssrn.com/abstract=1012075).

[18] Huii J.C., Options, Futures, and Other Derivatives (7th ed.), Prentice

Hall, 2007.

[19] Kirkpatrick C.D., Dahiquist J.R., Technical Analysis: The Complete

Resource for Financial Market Technicians (2nd ed.), FT Press, 2010.

[20] Mandeibrot N., Hudson R.L., The (Mis)Behavior of Markets: A Frac-

tal View of Risk, Ruin, and Reward, Basic Books, 2004.

More intriguing information

1. Chebyshev polynomial approximation to approximate partial differential equations2. A Multimodal Framework for Computer Mediated Learning: The Reshaping of Curriculum Knowledge and Learning

3. Locke's theory of perception

4. AN ECONOMIC EVALUATION OF THE COLORADO RIVER BASIN SALINITY CONTROL PROGRAM

5. The Economics of Uncovered Interest Parity Condition for Emerging Markets: A Survey

6. From Aurora Borealis to Carpathians. Searching the Road to Regional and Rural Development

7. What Contribution Can Residential Field Courses Make to the Education of 11-14 Year-olds?

8. The name is absent

9. Database Search Strategies for Proteomic Data Sets Generated by Electron Capture Dissociation Mass Spectrometry

10. Workforce or Workfare?