1200

1000

7000

6500

6000

5500

5000

4500

4000

3500

3000

2500

2000

0 500 1000 1500 2000 2500

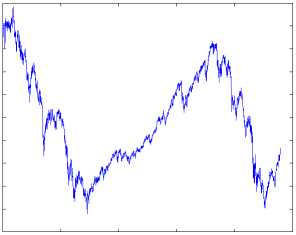

(a) Underlying asset: daily values of the CAC from

28 April 2000 until 18 September 2009

3000

inria-00457222, version 1 - 16 Feb 2010

800

600

400

200

Il ' ” All

∣W ' ....... λ∕⅜

It I ' l5" Æ M

s. ⅛ ....... ' А

0 200 400 600 800 1000 1200

0 200 400 600 800 1000 1200

(b) Option: CFU9PY3500 daily prices from 9 May (c) Option: CFU9CY3500 daily prices from 9 May

2009 until 18 September 2009

2009 until 18 September 2009

Figure 1: Daily data

4 Conclusion

Lack of space prevented us from examining more involved options, futures, and

other derivatives, than in Section 2.3. Subsequent works will do that, and also

introduce several time scales thanks to the nonstandard analytic framework of

the Cartier-Perrin theorem [4].

Acknowledgement. The authors would like to thank Frederic Hatt for stim-

ulating discussions.

References

[1] BechU T., Bertrand E., Nebenzahl J., L’analyse technique (6e ed.),

Economica, 2008.

[2] Bernhard P., El Farouq N., Thiery S., Robust control approach

to option pricing: a representation theorem and fast algorithm, SIAM J.

Control Optimiz., 46, 2280-2302, 2007.

More intriguing information

1. The name is absent2. On the job rotation problem

3. Multimedia as a Cognitive Tool

4. The Prohibition of the Proposed Springer-ProSiebenSat.1-Merger: How much Economics in German Merger Control?

5. The name is absent

6. Large-N and Large-T Properties of Panel Data Estimators and the Hausman Test

7. The name is absent

8. The name is absent

9. On the Relation between Robust and Bayesian Decision Making

10. Problems of operationalizing the concept of a cost-of-living index