in the revenue position since the Scottish variable rate of income tax (‘the tartan tax’) has not

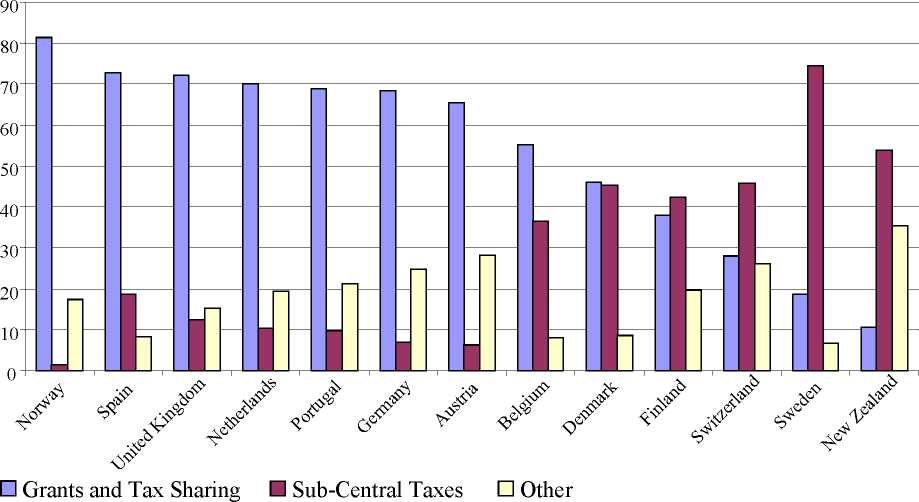

yet been employed). The graph shows that, amongst the unitary states, the UK relies mostly

on grants and not on locally-raised revenues from taxes and fees. Apart from the federal

states (Germany, Switzerland, the USA, Canada) unitary states such as Italy, France and the

Scandinavian countries rely less than the UK on central government grants to finance their

sub-central governments.

Figure 4: Composition of Sub-Central Government Revenues in 1995

as a percentage of General Government Revenues

Source: OECD (1999)

However, we should remember the caveat about tax sharing which also applied to Figure 1:

no distinction is made in Figure 3 between taxes under the control of sub-national

jurisdictions and tax-sharing schemes. If one were to strip out tax sharing from this figure,

federal countries like Germany and Austria would converge towards the unitary states.

Nevertheless, the UK’s relative position would still be one where reliance on grants is greater

13

More intriguing information

1. The name is absent2. Large-N and Large-T Properties of Panel Data Estimators and the Hausman Test

3. Human Rights Violations by the Executive: Complicity of the Judiciary in Cameroon?

4. Ronald Patterson, Violinist; Brooks Smith, Pianist

5. The name is absent

6. Word searches: on the use of verbal and non-verbal resources during classroom talk

7. DIVERSITY OF RURAL PLACES - TEXAS

8. Towards a framework for critical citizenship education

9. The name is absent

10. The name is absent