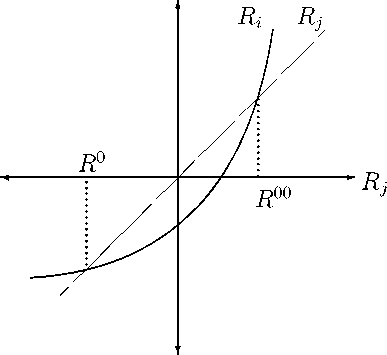

Figure 2

bl) Investor i demands higher ex-

pected portfolio return. His shar-

ing rule is convex relative to that

of investor j such that R and Rj

intersect once.

b2) Investor i has a higher risk

sensitivity. His sharing rule is

convex relative to that of in-

vestor j such that both inter-

sect twice.

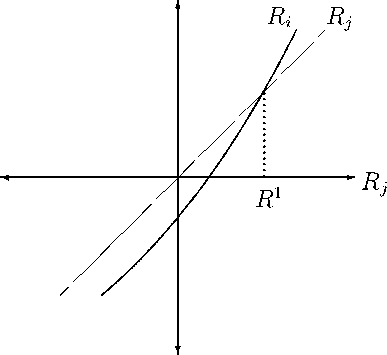

Proposition 6 is illustrated in Figure 2. If two investors i and j have

the same expected portfolio return and the same risk sensitivity, then their

portfolio returns are the same in every state. If investor i has a higher

risk sensitivity and/or demands a higher expected portfolio return, then her

sharing rule is convex relative to that of the other investor. The special cases

bl) and b2) will help to understand the intuition behind this result.

Proposition 6 bl) says that an investor i who ceteris paribus demands

a higher expected portfolio return than investor j chooses a portfolio such

that in the low states (Rj∙ < R1 ) her portfolio return is lower and in the high

states (Rj > R1 ) it is higher. Hence, a higher expected return forces her

26

More intriguing information

1. The name is absent2. Ein pragmatisierter Kalkul des naturlichen Schlieβens nebst Metatheorie

3. The name is absent

4. On Social and Market Sanctions in Deterring non Compliance in Pollution Standards

5. Crime as a Social Cost of Poverty and Inequality: A Review Focusing on Developing Countries

6. Rent Dissipation in Chartered Recreational Fishing: Inside the Black Box

7. On the Desirability of Taxing Charitable Contributions

8. The name is absent

9. The name is absent

10. Financial Market Volatility and Primary Placements