Percent Percent Percent

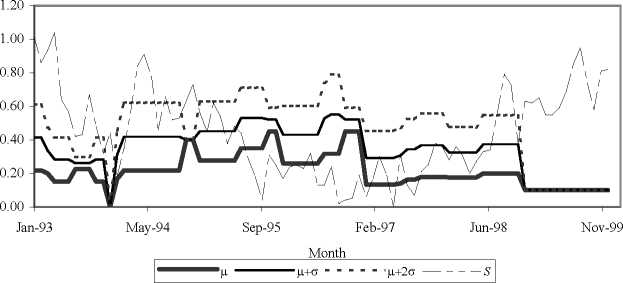

Panel A: AA-Rated Bonds

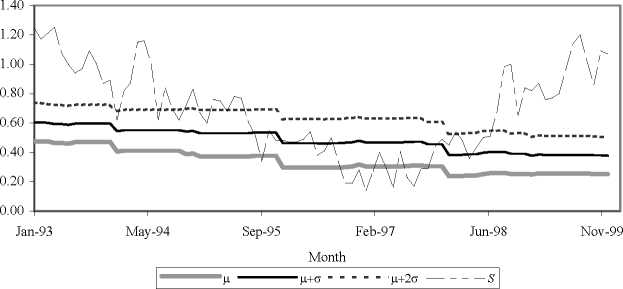

Panel B: A-Rated Bonds

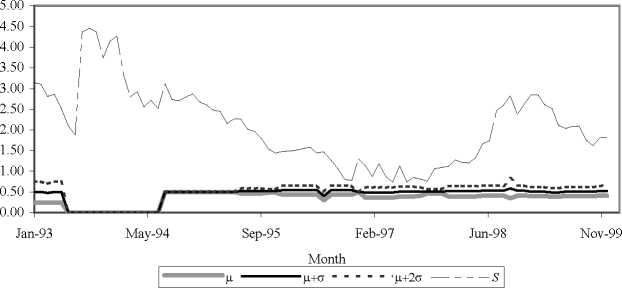

Panel C: BBB-Rated Bonds

Figure 1. Moneyness of the doomsday call provision. To determine

the moneyness of the doomsday call provision, we compare the

doomsday spread to the yield spread. Based on a sample of doomsday

spreads of long bonds for each month during the 01:1993-12:1999

period, for each rating category, we plot the yield spread on the

corresponding long-term index ( 5), the average doomsday spread (μ),

the average doomsday spread plus one standard deviation (μ+σ), and

the average doomsday spread plus two standard deviations ( μ+2σ).

46

More intriguing information

1. Infrastructure Investment in Network Industries: The Role of Incentive Regulation and Regulatory Independence2. Pupils’ attitudes towards art teaching in primary school: an evaluation tool

3. The name is absent

4. A NEW PERSPECTIVE ON UNDERINVESTMENT IN AGRICULTURAL R&D

5. Three Strikes and You.re Out: Reply to Cooper and Willis

6. A Location Game On Disjoint Circles

7. The name is absent

8. The name is absent

9. The name is absent

10. Evaluating the Success of the School Commodity Food Program