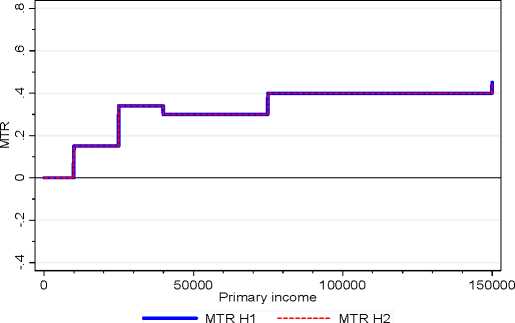

personal income is combined with the Low Income Tax Offset (LITO). The LITO has

the effect of raising the zero rated threshold of the personal income tax rate schedule

from $6000 to $10,000 and the MTR on income from $25,001 to $40,000 from 30

cents to 34 cents in the dollar. 10 Because the tax base is still individual income and

the partners in the H2 household earn the same incomes, the graph shows a single

MTR profile for both partners in the H2 household.

Figure 1a MTR schedule + LITO

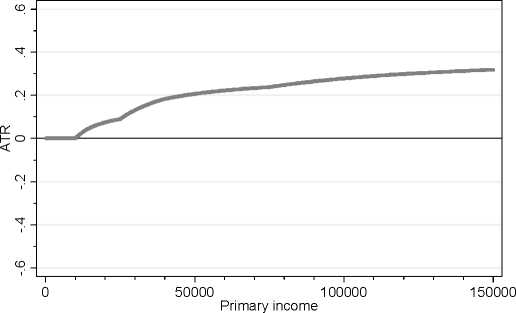

Figure 1b ATRs: MTR schedule + LITO

------ ATRH H1 --------- ATR2 H2

— ATRH H2

Figure 1b plots the ATR profile. Again, there is a single profile because the tax base

is individual income. Note, however, that both members of the H2 household pay tax,

and so at any given level of primary income, the household pays twice as much tax as

10 The LITO is in fact an entirely redundant policy instrument that serves only to reduce the

transparency of the true MTR schedule, with a rate of 34 cents in the dollar on incomes from $25,001

to $40,000, depicted in Figure 1.

More intriguing information

1. STIMULATING COOPERATION AMONG FARMERS IN A POST-SOCIALIST ECONOMY: LESSONS FROM A PUBLIC-PRIVATE MARKETING PARTNERSHIP IN POLAND2. Are Public Investment Efficient in Creating Capital Stocks in Developing Countries?

3. Delayed Manifestation of T ransurethral Syndrome as a Complication of T ransurethral Prostatic Resection

4. The name is absent

5. The name is absent

6. On s-additive robust representation of convex risk measures for unbounded financial positions in the presence of uncertainty about the market model

7. The name is absent

8. The name is absent

9. IMPROVING THE UNIVERSITY'S PERFORMANCE IN PUBLIC POLICY EDUCATION

10. The Role of State Trading Enterprises and Their Impact on Agricultural Development and Economic Growth in Developing Countries