The criterion function depends on the Zs, namely variables correlated with the decision of

introducing innovations, such as R&D expenditure at the beginning of the sample period and the

other determinants of innovation, including age and the share of temporary workers.

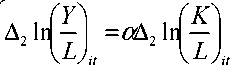

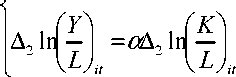

To estimate the parameters δ' we observe that the expected value E(D1)=P(D1=1)=P(δ,Zit+ωit>0)

is the probability of being an innovative firm. If the error term ωit is assumed with E(ωit) = 0 and

V(ωit ) = 1 the (first stage) estimation method applied is the probit maximum likelihood.

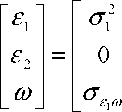

Usually equation (6) is estimated separately for the two regimes, whose idiosyncratic errors are

correlated with ωit, according to the covariance matrix:

Var

0

σ22

σ

ε2

σε1

σε2

1

In this case we need to introduce corrections for the error conditional mean as in (8) and (8’):

Ε(ε1it | D1 = 1) = Ε(σεωωit | δZit + ωit

1it 1 ε1ω it it it

-σ

ε1

Φ(δZit )

Φ(δ zu )

(8)

Ε(ε2it | D2 = 1) = Ε(σε ωωit | δZit + ωit

2it 2 ε2ω it it it

Φ(δZit )

*ω 1 -Φ(δzu )

(8’)

where φ(∙) and Φ(∙) are, respectively, the standard normal density and cumulative distribution

functions. To calculate (8) and (8’) notice that we used the conditional distribution of ε given ω.

This is normal with mean E(εjit | ωit) = σεj1ωωit and variance V(εjit | ωit) = σj2-σ2εjω. Given (6)-(8’), our

specification becomes:

n l ( Temporary ΦδZit )

+β +γlAge + μ∣: ∖-2 σ + U..

if D1 =1

if D1 =0

(9)

_ , ( Temporary Φ(δZit )

+β2 + γ2 Age + μ2∖-------H +σz> —-—i—+u2i.

2 2 i 2 ε1ω 2it

∖ L Jit-2 1-φ(δ Zit )

This system of equations can be estimated consistently with OLS (second stage) after substituting

the estimate of δ'Z in the correction terms (derived from first stage probit estimation).7

7

Building on Maddala (1983) we could simplify equation (9) simultaneously, adding the correction term, i.e. the sum

of (8) + (8’), for the whole sample:

12

More intriguing information

1. Design and investigation of scalable multicast recursive protocols for wired and wireless ad hoc networks2. BODY LANGUAGE IS OF PARTICULAR IMPORTANCE IN LARGE GROUPS

3. The Functions of Postpartum Depression

4. GENE EXPRESSION AND ITS DISCONTENTS Developmental disorders as dysfunctions of epigenetic cognition

5. Globalization and the benefits of trade

6. The name is absent

7. Estimation of marginal abatement costs for undesirable outputs in India's power generation sector: An output distance function approach.

8. Outsourcing, Complementary Innovations and Growth

9. Federal Tax-Transfer Policy and Intergovernmental Pre-Commitment

10. The name is absent