Uncertain Productivity Growth

4 TIMING & COMPARATIVE STATICS

By integrating the probability density function (69) it is possible to derive the corresponding

cumulative distribution functions as

G(T*,⅞A*) = N

+ (α

1 σ2)T*

+e

(α

1 σ2)t

(74)

with ⅛ << and i ∈{E,F}.

* *■*

Expected Market Entry Time Te, Tf

(a) ¾ < ⅛F, α = 0.04,⅛0 = 1,σ = 0.1, but

FF (ð) > FE (ð) with κ = 1

(b) ¾ < ⅛F, α = 0.04,⅛0 = 1,σ = 0.16, but

FF (tf) > FE (tf) with κ = 1

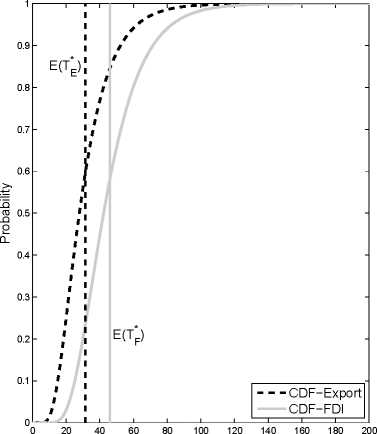

Figure 8: Cumulative Distribution Functions of Ti*.

Panel a) in figure 8 represents the cumulative distribution functions of both investment strategies

for a relative cost constellation which leads to a productivity cut-off ranking with tf*E < &р. The

vertical dashed line represents the export mode’s expected market entry time and the s-shaped

curve its cumulative distribution function. The continuous curves represent the FDI mode. In

the underlying example the export mode exhibits a first-order stochastic dominance over the FDI

strategy. Differently expressed, for any market entry time Ti* , the probability of market entry

through exports will always be higher than in the FDI case. However, for the chosen relative cost

pattern, the FDI mode exhibits a higher option value (see figure 7, areas F2 , F3) and therefore

32

More intriguing information

1. Global Excess Liquidity and House Prices - A VAR Analysis for OECD Countries2. Long-Term Capital Movements

3. Announcement effects of convertible bond loans versus warrant-bond loans: An empirical analysis for the Dutch market

4. HACCP AND MEAT AND POULTRY INSPECTION

5. Putting Globalization and Concentration in the Agri-food Sector into Context

6. DIVERSITY OF RURAL PLACES - TEXAS

7. The name is absent

8. Linkages between research, scholarship and teaching in universities in China

9. Convergence in TFP among Italian Regions - Panel Unit Roots with Heterogeneity and Cross Sectional Dependence

10. The Economics of Uncovered Interest Parity Condition for Emerging Markets: A Survey