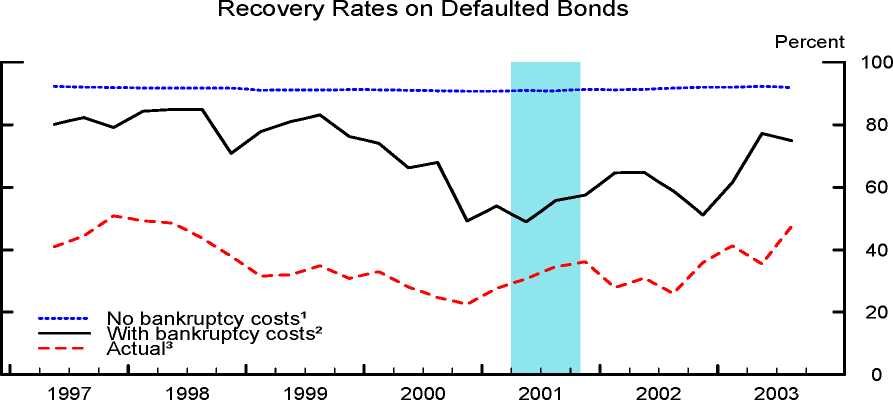

Figure 8

1 Average model-implied recovery rate with μ = 0, weighted by the book value of bonds outstanding.

2 Average model-implied recovery rate with estimated μ , weighted by the book value of bonds

outstanding.

3 Average recovery rate at default weighted by the book value of the defaulted bond issue

(four-quarter moving average).

cyclically, amplifying the swings in borrowing and, consequently, in investment and

output.

Figure 9 shows the cyclical behavior of the model-implied external finance pre-

mium calculated using the solutions for ω*t and σ*t and our estimates of the bankruptcy

cost parameter μt. Smoothing through the Russian default in late 1998, the model-

implied external finance premium was close to zero across the entire cross-section of

firms until the end of 1999. As stock prices began to slide in early 2000, causing a

decline in firms’ net worth (i.e., market capitalization) and an increase in corporate

leverage, the external finance premium rose sharply, and the increase is economically

significant. Firms that account for a half of aggregate sample sales experienced an

increase in the external finance premium of at least 150 basis points, while firms that

account for one quarter of aggregate sample sales faced an increase in the external fi-

nance premium of more than 300 basis points. The external finance premium started

to decline at the end of the NBER-date recession but then jumped up again at the

end of 2002 in response to concerns about corporate governance.

To investigate the interaction between the cyclical behavior of our estimates of

μ and the dynamics of the external finance premium over the latest business cycle,

27

More intriguing information

1. The name is absent2. Climate Policy under Sustainable Discounted Utilitarianism

3. The constitution and evolution of the stars

4. Importing Feminist Criticism

5. The name is absent

6. Dual Inflation Under the Currency Board: The Challenges of Bulgarian EU Accession

7. Long-Term Capital Movements

8. A NEW PERSPECTIVE ON UNDERINVESTMENT IN AGRICULTURAL R&D

9. Implementation of a 3GPP LTE Turbo Decoder Accelerator on GPU

10. On Social and Market Sanctions in Deterring non Compliance in Pollution Standards