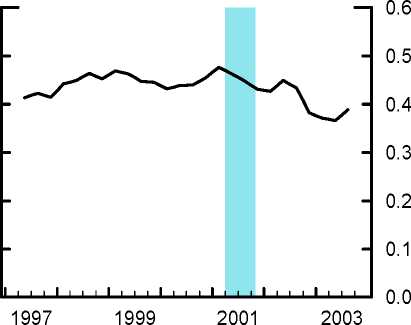

Figure 10

Idiosyncratic Risk and Probability of Default

Median Model-Implied σ

Note. Medians are weighted by real sales.

Median Year-Ahead EDF

Percent

0.6

0.5

0.4

0.3

0.2

0.1

0.0

1997 1999 2001 2003

5.2 Excluding Credit Rating Effects

The main reason for including credit ratings in our credit spread equation 12 is

that they represent a reasonable proxy for liquidity factors. As already mentioned,

corporate bonds can include a liquidity premium due to the fact that markets are

at times relatively thin and illiquid. To analyze whether liquidity factors are indeed

a significant component of observed credit spreads and to shed some light on their

interaction with financial market frictions, we reestimate the time-varying bankruptcy

parameter μ without including credit rating effects.

As shown in the upper panel of Figure 11, excluding credit ratings generates a

significantly larger estimates of the bankruptcy parameter μt, though the time-series

pattern remains the same.27 According to Table 3, the fit of the model with industry

effects alone is about half as good as the benchmark specification that includes both

fixed credit rating and industry effects. This suggests that credit ratings might be

picking up an important component of the residual spread in equation 12, which

27Although industry effects are statistically significant in the benchmark specification—at least

during the latter half of our sample period—their exclusion has a negligible effect on the estimates

of μ.

30

More intriguing information

1. Estimating the Economic Value of Specific Characteristics Associated with Angus Bulls Sold at Auction2. Personal Experience: A Most Vicious and Limited Circle!? On the Role of Entrepreneurial Experience for Firm Survival

3. How to do things without words: Infants, utterance-activity and distributed cognition.

4. What Contribution Can Residential Field Courses Make to the Education of 11-14 Year-olds?

5. The name is absent

6. The name is absent

7. Education and Development: The Issues and the Evidence

8. Survey of Literature on Covered and Uncovered Interest Parities

9. Citizenship

10. Modelling the health related benefits of environmental policies - a CGE analysis for the eu countries with gem-e3