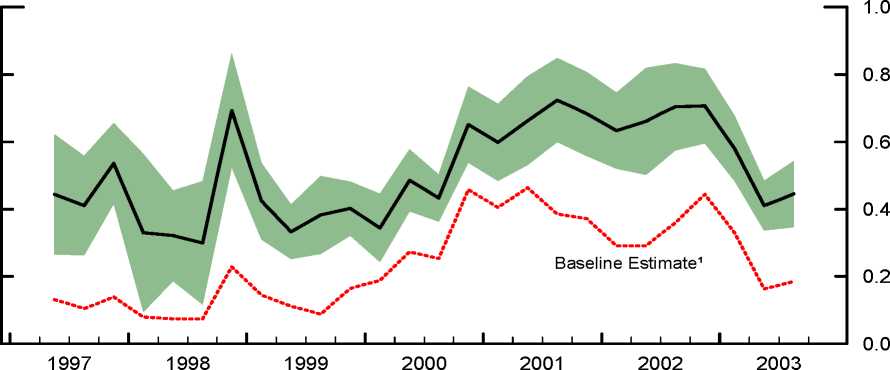

Figure 11

Estimates Without Credit Rating Effects

NLLS Estimates of the Bankruptcy Cost Parameter μ

Note. The shaded region represents +/- two standard error bands computed using a

heteroscedasticity-consistent asymptotic covariance matrix. The model includes fixed industry

(3-digit NAICS) effects.

1 See Figure 6.

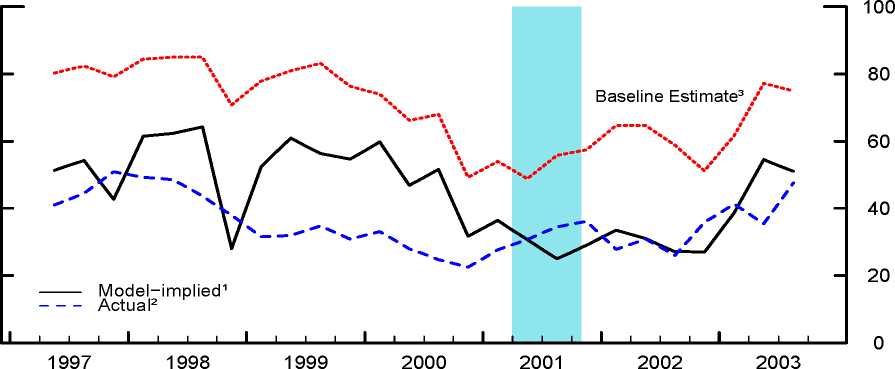

Recovery Rates on Defaulted Bonds

Percent

1 Average model-implied recovery rate weighted by the book value of bonds outstanding.

2 Average recovery rate at default weighted by the book value of the defaulted bond issue

(four-quarter moving average).

3 See Figure 7.

31

More intriguing information

1. Searching Threshold Inflation for India2. Tourism in Rural Areas and Regional Development Planning

3. Happiness in Eastern Europe

4. The name is absent

5. Fiscal Insurance and Debt Management in OECD Economies

6. Integration, Regional Specialization and Growth Differentials in EU Acceding Countries: Evidence from Hungary

7. The name is absent

8. The name is absent

9. From Aurora Borealis to Carpathians. Searching the Road to Regional and Rural Development

10. The name is absent