12

W. K. Hardle, R. A. Moro, and D. Schafer

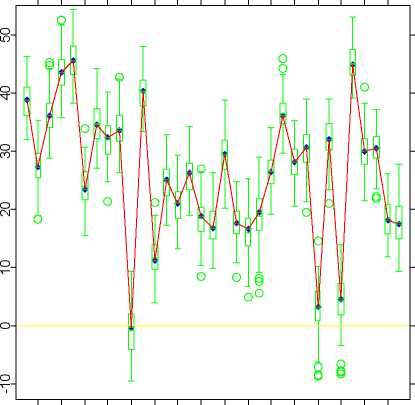

AR (Model: SVM K*)

2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32

Variable No.

Fig. 8. Accuracy ratios for univariate SVM models. Box-plots are estimated basing

on 100 random subsamples. The AR for the model containing only random variable

K10 is zero.

5 Conversion of Scores into PDs

There is another way to look at the company score. It defines the distance

between companies in terms of the distance to the boundary between the

classes. The lower is the score, the farther is a company from the class of

bankrupt companies, therefore, we can assume, the lower PD it must have.

This means that the dependence between scores and PDs is assumed to be

monotonous. This is the only kind of dependence that was assumed in all

rating models mentioned in this chapter and the only one we use for PD

calibration.

The conversion procedure consists of the estimation of PDs for the obser-

vation of the training set with a subsequent monotonisation (step one and

two) and the computation of a PD for some new company (step three).

Step one is the estimation of PDs for the companies of the training set.

We used kernel techniques to preliminary evaluate PDs for observation i from

the training set, i = 1, 2, . . . , n:

--------

PD(xi) =

П=1к Kh(xi,xj)I{yj = 1}

n=1K Kh(xi ,xj )

(11)

More intriguing information

1. The name is absent2. The name is absent

3. Applications of Evolutionary Economic Geography

4. Exchange Rate Uncertainty and Trade Growth - A Comparison of Linear and Nonlinear (Forecasting) Models

5. Dual Inflation Under the Currency Board: The Challenges of Bulgarian EU Accession

6. Work Rich, Time Poor? Time-Use of Women and Men in Ireland

7. The name is absent

8. Epistemology and conceptual resources for the development of learning technologies

9. The name is absent

10. A production model and maintenance planning model for the process industry