10

W. K. Hardle, R. A. Moro, and D. Schafer

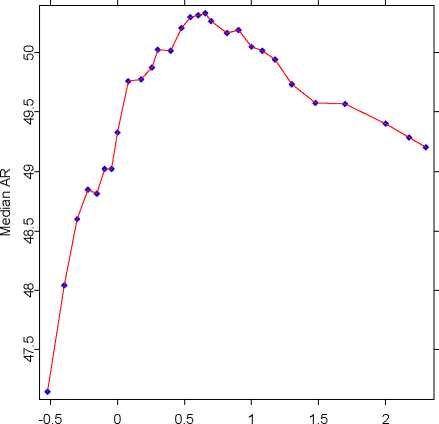

Accuracy Ratio

log10(r)

Fig. 7. The relationship between an accuracy measure (AR) and the coefficient r

in the SVM formulation. Higher r’s correspond to less complex models. The median

ARs were estimated on 100 bootstrapped subsamples of 500 solvent and 500 insol-

vent companies both in the training and validation sets. A bivariate SVM with the

variables K5 and K29 was used. We will be using r = 4 in all SVMs used in this

chapter.

We have also conducted experiments with subsamples of the size of 5000

observations. The change of median was extremely small (one-two orders of

magnitude smaller than the interquartile range). The interquartile range got

narrower as it was expected, i.e. the difference between models with bigger

samples is only more statistically significant. Thus, proving that if the differ-

ence is significant on a sample of 1000 observations, it can be guaranteed that

this will remain so for bigger samples.

The SVM based on variables K5, K29, K7, K33, K18, K21, K24, K33 and

K9 attains the highest median AR of around 60.0%. For comparison we plot

an improvement in AR for the SVM vs. DA and logit regression on the same

100 subsamples. The data used in the DA and logit models were processed

as following: if xi < q0.05 (xi) then xi = q0.05 (x) and if xi > q0.95 (xi) then

xi = q0.95(xi); i = 1, 2, . . . , 8; qα(xi) is an α quantile of xi. Thus, the DA and

logit regression applied were robust versions not sensitive to outliers. Without

such a procedure the improvement would be much higher.

More intriguing information

1. Foreword: Special Issue on Invasive Species2. Healthy state, worried workers: North Carolina in the world economy

3. Emissions Trading, Electricity Industry Restructuring and Investment in Pollution Abatement

4. The name is absent

5. Fortschritte bei der Exportorientierung von Dienstleistungsunternehmen

6. The name is absent

7. The name is absent

8. The English Examining Boards: Their route from independence to government outsourcing agencies

9. The name is absent

10. Macroeconomic Interdependence in a Two-Country DSGE Model under Diverging Interest-Rate Rules