Differentiating (18) with respect to Rm gives

d(ωma

- ωms)

dRm

-Rmfma(Rm) + Rmfms (Rm) - (1 - Fma(Rm))

+Rmfma (Rm) + (1 - Fms (Rm)) - Rmfms (Rm)

Fma (Rm )

Fms (Rm).

From (17) it follows d(ωma~ωms) > 0 for Rm < Dm and d(ωma-ωms) < 0 otherwise. This,

dRm 2 dRm

along with ωma - ωms =0 both for Rm = 0 and for Rm = Dm implies ωma - ωms > 0for

all Rm ∈ [0,Dm]. Q.E.D.

Proof of Proposition 2

The demand for liquidity of the merged banks, xm = δ1 Dm + δ2 Dm, has density function

as in (16). Using Leibniz’s rule, the equality Dm = Rm + L1 + L2, and the ratio km

Rm

Dm

from (11) we can express the first order condition dRm = 0 as

8 km - 4km + 1 = rD for km ≤ 1/2

(19)

8(1 - km)3 = rD for km > 1/2.

The term on the LHS of the equalities is the marginal benefit of increasing the reserve-

deposit ratio, that is the reduction in the expected need of refinancing induced by a marginal

increase of the reserve ratio. The term on the RHS of the equalities is the ratio between the

marginal cost of raising reserves rD and the marginal cost of refinancing rI. From (19), we

obtain:

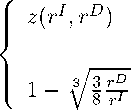

km

for rI ≤ 3rD

for rI > 3rD,

(20)

where z(rI, rD) is the solution of the equation z3 — 3z2 + 8(1 — rD) = 0 in the interval (0, ∣]

increasing in the ratio rD. Since f(0) > 0, f(1/2) < 0 and f0(z) < 0, z(rI,rD) is the unique

real solution.

To compare km with ksq, we rearrange ksq given in (10) as

rD

(1 - ksq) = r∣γ-, (21)

where, as before, the LHS is the marginal benefit of increasing the reserve-deposit ratio and

the RHS is the ratio between the marginal cost of raising deposits and holding reserves rD

and the marginal cost of refinancing rI .

31

More intriguing information

1. Industrial Cores and Peripheries in Brazil2. The name is absent

3. Understanding the (relative) fall and rise of construction wages

4. Before and After the Hartz Reforms: The Performance of Active Labour Market Policy in Germany

5. The name is absent

6. The name is absent

7. Yield curve analysis

8. The name is absent

9. On the origin of the cumulative semantic inhibition effect

10. Biological Control of Giant Reed (Arundo donax): Economic Aspects