4 A sectoral analysis

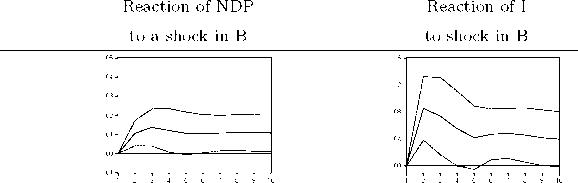

Figure 3: Impulse Responses for Net Domestic Product and Bank Lending, and Investment and Bank

Lending

Panel A

Panel B

Note: The solid lines trace the impulse responses of net domestic product

(NDP) and investment (I) to shocks in bank lending (B) for the years 1870

to 1912.

Table 4: Variance Decomposition for Net Domestic Product and Bank Lending, and Investment and

Bank Lending

Years

Variance Decomposition 5 10

NDP variance due to B (in percent) 20.777 21.045

[10.648] [11.186]

I variance due to B (in percent) 25.256 25.690

_____________________________________________[12.860] [13.955]

Note: The variance decomposition of the forecast error is

shown for the three-variable VAR, including net domestic

product (NDP), investment (I) and bank lending (B) for the

years 1870 to 1912. The values in parentheses indicate the

standard deviation.

4 A sectoral analysis

The findings in the previous sections largely confirmed earlier research on historical data in

Germany and other countries. A key question that we would like to address in the present

paper, is to understand which sectors of the economy benefited most strongly from the pos-

itive link between bank lending and growth. In the literature on today’s emerging markets,

pronounced sectoral asymmetries are often found, and we find it very interesting to compare

how the growth process in 19th century Germany relates to the experiences of the emerging

markets of the last 20 to 30 years. We therefore also investigate the sectoral differences in the

responses of output to aggregate lending in this section.

In the literature on financial development in emerging markets, sectors are typically classi-

fied as small (and non-tradable) or large (and tradable). The motivation for this classification

10

More intriguing information

1. The name is absent2. The name is absent

3. CREDIT SCORING, LOAN PRICING, AND FARM BUSINESS PERFORMANCE

4. ARE VOLATILITY EXPECTATIONS CHARACTERIZED BY REGIME SHIFTS? EVIDENCE FROM IMPLIED VOLATILITY INDICES

5. Sex-gender-sexuality: how sex, gender, and sexuality constellations are constituted in secondary schools

6. Income Taxation when Markets are Incomplete

7. Visual Artists Between Cultural Demand and Economic Subsistence. Empirical Findings From Berlin.

8. DEMAND FOR MEAT AND FISH PRODUCTS IN KOREA

9. DETERMINANTS OF FOOD AWAY FROM HOME AMONG AFRICAN-AMERICANS

10. The Cost of Food Safety Technologies in the Meat and Poultry Industries.