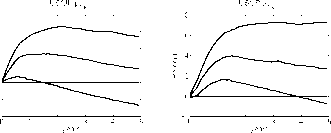

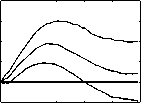

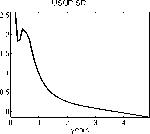

US-Ger

12

10

8

EE

US/GE ρ0,k

00 1 2 3 4 5

years

US-UK

US-Japan

8

6

4

8

6

c 4

BIG

4

2

0

-2

-4

4

2

O

O

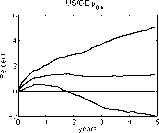

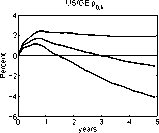

US/JP ρ0,k

20 1 2 3 4 5

years

US/JP ρ0,k

Eich.-Evans

-4

-60 1 2 3 4 5

years

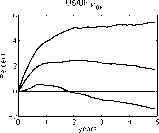

US/UK ρtlk

3

2

1

O

-1

-2

-3

0 1 2 3 4 5

years

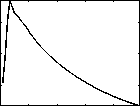

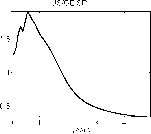

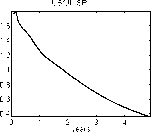

Figure 9: Impulse responses for the forward discount premium ρk , conditional

on a US monetary policy contraction.

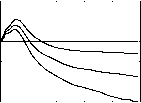

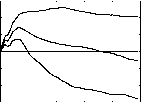

EE

BIG

Eich.-Evans

US-Ger

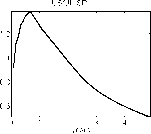

US/GE SR

US-UK

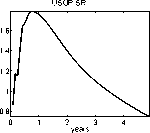

US/UK SR

V

0 12 3 4

years

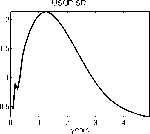

US-Japan

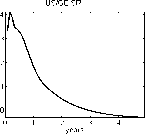

Figure 10: Impulse responses for the Sharpe ratio of a Bayesian investor,

conditional on a US monetary policy contraction.

43

More intriguing information

1. Behaviour-based Knowledge Systems: An Epigenetic Path from Behaviour to Knowledge2. Pricing American-style Derivatives under the Heston Model Dynamics: A Fast Fourier Transformation in the Geske–Johnson Scheme

3. The name is absent

4. Deletion of a mycobacterial gene encoding a reductase leads to an altered cell wall containing β-oxo-mycolic acid analogues, and the accumulation of long-chain ketones related to mycolic acids

5. DETERMINANTS OF FOOD AWAY FROM HOME AMONG AFRICAN-AMERICANS

6. The name is absent

7. The name is absent

8. L'organisation en réseau comme forme « indéterminée »

9. Langfristige Wachstumsaussichten der ukrainischen Wirtschaft : Potenziale und Barrieren

10. The Nobel Memorial Prize for Robert F. Engle