central government, arguably the joint taxes are very similar to a block grant. Countries with

such arrangements give very limited fiscal autonomy to their regional or local governments.

Also, it should be recognised that, even where the yield of local taxes is returned fully to the

sub-central governments, central government may still be able to limit the degree to which

this fiscal autonomy is exercised.

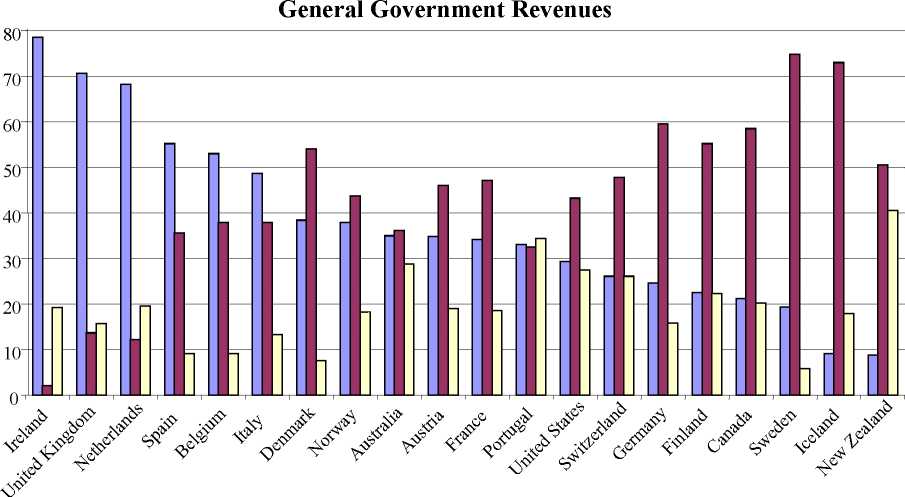

Figure 1: Composition of Sub-Central Government Revenues as a Percentage of

□ Grants □ Taxes □ Other

Source: IMF Government Financial Statistics 2001

Note: Figures relate to 2000 for Canada, Denmark and New Zealand; to 1999 for Australia, Austria,

Sweden, Switzerland and the USA; to 1998 for Belgium, Finland, Germany, Iceland, Portugal,

Norway, UK; and to 1997 for France and the Netherlands.

In order to shed more light on the degree of fiscal autonomy enjoyed by lower levels of

government, one has to look in detail at the extent to which sub-central governments can

actually control taxation. A more systematic analysis of this is possible following the

classification framework for local taxation developed by the Working Party on Tax Policy

Analysis and Tax Statistics of the OECD Committee on Fiscal Affairs. This has resulted in

the publication of a number of studies on local taxation (see OECD 1999, 2001), which allow

More intriguing information

1. Langfristige Wachstumsaussichten der ukrainischen Wirtschaft : Potenziale und Barrieren2. Understanding the (relative) fall and rise of construction wages

3. Enterpreneurship and problems of specialists training in Ukraine

4. Exchange Rate Uncertainty and Trade Growth - A Comparison of Linear and Nonlinear (Forecasting) Models

5. The name is absent

6. The name is absent

7. The name is absent

8. AN IMPROVED 2D OPTICAL FLOW SENSOR FOR MOTION SEGMENTATION

9. Healthy state, worried workers: North Carolina in the world economy

10. Notes on an Endogenous Growth Model with two Capital Stocks II: The Stochastic Case