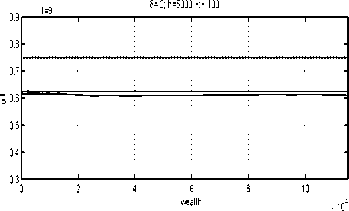

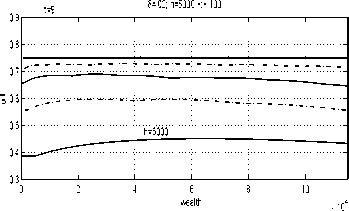

Fig. 9. Approximating strategies for t = 9

(5=.2).

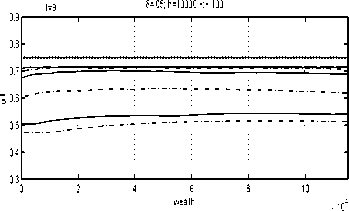

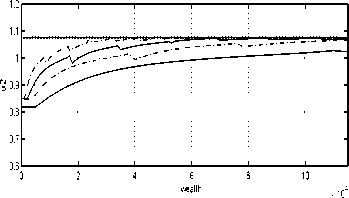

Fig. 11. Approximating strategies for t = 9

(5 = .05).

t=9 δ=.1; h=10000 -:- 100

0.9 I-------------------------------------1-------------------------------------1-------------------------------------1-------------------------------------1-------------------------------------1---------------------------

0.8-...............i.................:.................i................∖................i...........-

0.7 ......:.................

S 0.6-...............i.................:.................i................∖................i...........-

0.5-............... :.................:................:................ -

0.4-...............i.................:.................i................∖................i...........-

0.3∣-------------------------------------i-------------------------------------i-------------------------------------i-------------------------------------i-------------------------------------i---------------------------

0 2 4 6 8 10

wea∣th x 104

Fig. 10. Approximating strategies for t = 9

(5=.1).

Fig. 12. Approximating strategies for t = 9

(5= .02 “small”).

Indeed, the gap between the optimal strategy and

the approximating strategies for t = O is narrow

for 5 = .2 and closes for 5 = .1 (for reasonably

small h) whereas, for t = 9, it narrows down only

for smaller 5s, see Figures 11 and 12. This is to

be expected because the optimal U2(T) = ∞,

and U2(T) = ∞ (see (32) and (30)), which is

impossible to reproduce numerically.

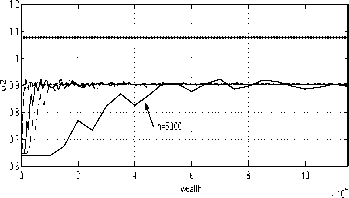

Figure 13 shows the wealth and strategy reali-

sations for 5 = .05 and h = 100. They look

very similar to the optimal ones in Figure 4. The

simulation of 2000 noise realisations and the appli-

cation of the approximating policy rules computed

for the same parameters (i.e., 5 = .05 and h =

100) resulted in the utility distribution (integrated

with the time simulation step equal to .025) shown

in Figure 14.

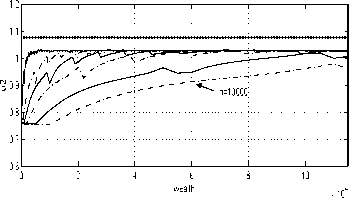

The mean discounted utility is J = 715.4 (98.9 %

optimal) and the corresponding standard devia-

tion is 161. However, the portfolio performance

10

More intriguing information

1. Evaluation of the Development Potential of Russian Cities2. Conflict and Uncertainty: A Dynamic Approach

3. Skills, Partnerships and Tenancy in Sri Lankan Rice Farms

4. Towards a Strategy for Improving Agricultural Inputs Markets in Africa

5. The migration of unskilled youth: Is there any wage gain?

6. Public-Private Partnerships in Urban Development in the United States

7. The name is absent

8. Computational Batik Motif Generation Innovation of Traditi onal Heritage by Fracta l Computation

9. Implementation of Rule Based Algorithm for Sandhi-Vicheda Of Compound Hindi Words

10. Tourism in Rural Areas and Regional Development Planning