Fig. 6. Strategy convergence.

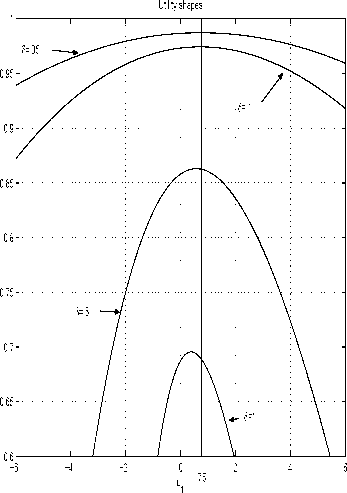

The vertical line t⅛=.75 shows where the utility

maximum “should” be, for it is known from Figure

2 that the optimal strategy is t⅛=.75, indepen-

dent of time. It is clear from the figure that the

discretised model strategy uχrι(δ) converges to the

optimal strategy as <) → 0. Again, any reasonable

approximation requires δ < .1.

Another point to remember is that the time step

δ should be large enough for the process to move

beyond the adjacent state i.e., δ∖f. ∣ > h. On the

other hand, as shown above, δ should be small for

high accuracy of the approximating solutions.

The convergence. There are various ways in

which the goodness of a numerical solution can

be evaluated. The most “objective” one would

perhaps be to look at the average discounted total

utility J generated by the application of an ap-

proximated optimal numerical solution to the con-

tinuous model. However, as evident from Figure 4,

the portfolio performance is very “volatile” and

the standard deviation of utility distribution is

large. Therefore, using J thus computed is difficult

to judge which solution is best.

We will first evaluate the convergence by compar-

ing the approximating policy profiles (Figures 7 -

12), to the optimal ones (Figure 2).9 Then, we

9 Remember that because of the model re-scaling, if l'2

was linear (Figure 2) u2 will be horizontal.

will generate a few realisation profiles to compare

them to those of Figure 4 and, eventually, we will

compute the corresponding utility distribution.

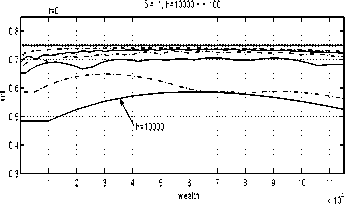

S = .2; h=10000 -:- 100

0.81-

0.7

160

0.5-

0.4-

1 2 3 4 5 6 7 8 9 10 1 1

wealth x 104

0.3

0.35

0.3

025

0.2

0.15

• h=10000

0.11-------------1-------------1-------------1-------------1-------------1-------------1-------------1-------------1-------------1-------------1-------------1_|

1 2 3 4 5 6 7 8 9 10 1 1

wealth χ104

Fig. 7. Approximating strategies for t = 0

(5=.2).

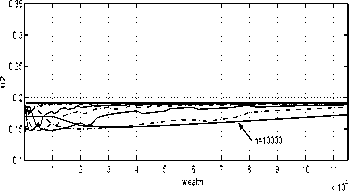

Examine the policy rules shown in Figures 7 -

12. The bold dotted lines correspond to opti-

mal strategies (compare Figure 2). One can see

that the strategy convergence is more difficult

to achieve for later times (t = 9) than at the

beginning of the horizon (t = 0).

Fig. 8. Approximating strategies for t = 0

(5=.1).

More intriguing information

1. Fertility in Developing Countries2. Strategic monetary policy in a monetary union with non-atomistic wage setters

3. The name is absent

4. Naïve Bayes vs. Decision Trees vs. Neural Networks in the Classification of Training Web Pages

5. DETERMINANTS OF FOOD AWAY FROM HOME AMONG AFRICAN-AMERICANS

6. The name is absent

7. The name is absent

8. Inhimillinen pääoma ja palkat Suomessa: Paluu perusmalliin

9. The Environmental Kuznets Curve Under a New framework: Role of Social Capital in Water Pollution

10. On s-additive robust representation of convex risk measures for unbounded financial positions in the presence of uncertainty about the market model