We can write the cdf F and the quantile function F~1 corresponding to a skew

density f of an X distribution using the cdf G and the quantile function G~1 of the

symmetric density. We have

F(x) =

for X < 0,

for X > 0.

for the cdf and

f ⅛G^1 [(1 + κ2)⅞] for x < 0,

F~1(x) = < L 2J ~

ɪ-κG~1 [(1 + κ-2)++ for x > 0,

for the quantile function. Moreover, the moments of order r, r = 1, 2,..., can be written

as

/.'r÷ ' 4- (~ ŋ

E(Xr) = 2E+(Xr)-------K~(r+1) ,

κ + ∑

where oo

E+(Xr) = / xrg(x)dx

Jo

is the r-th moment of the symmetric distribution truncated to positive values. Clearly

E+(Xr) assumes the value of the r-th moment of the symmetric distribution divided

by 2 when r is even.

On the basis of these formulations, we present the main characteristics of the dis-

tributions considered (for details see, among others, Ayebo and Kozubowski, 2003;

Lambert and Laurent, 2001; Palmitesta and Provasi, 2004).

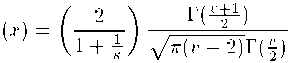

Skew Student-t. A random variable X has a skew Student t distribution (SST) if the

parameters к > 0 and v > 2 exist such that the pdf of X is

2s8nC)κ2'

(v÷l)∕2

where Γ(∙) indicates the gamma fucntion. If к = 1, the distribution is symmetric on

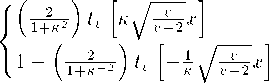

zero and has zero mean and unit variance. The cdf of X is given by

for x < 0,

for x > 0,

Γ(4±l) / 2∖- C + l)∕2

where

Tsst(«) =

t+)= ЛгД ι+- dw

J-00 √≡Γ(+ V V J

is the cdf of the unsealed Student t with υ degrees of freedom.

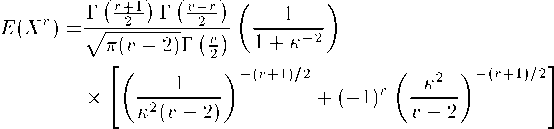

The moments of order r, r = 1, 2,..., of the SST distribution are:

and exist when v > r.

More intriguing information

1. SOME ISSUES IN LAND TENURE, OWNERSHIP AND CONTROL IN DISPERSED VS. CONCENTRATED AGRICULTURE2. The name is absent

3. MULTIPLE COMPARISONS WITH THE BEST: BAYESIAN PRECISION MEASURES OF EFFICIENCY RANKINGS

4. The Folklore of Sorting Algorithms

5. The Works of the Right Honourable Edmund Burke

6. NEW DEVELOPMENTS IN FARM PRICE AND INCOME POLICY PROGRAMS: PART I. SITUATION AND PROBLEM

7. The name is absent

8. The Dynamic Cost of the Draft

9. The name is absent

10. The Economic Value of Basin Protection to Improve the Quality and Reliability of Potable Water Supply: Some Evidence from Ecuador