Fig. 20. Yield location and spread measures.

To quantify a risk level associated with this policy,

two popular risk measures, Valuc-at-Risk (VaR)

and Conditional Valuc-at-Risk15 (CVaR) can be

approximately calculated from the histogram. The

/J-VaR of a portfolio is the lowest- amount- a such

that, with probability β the loss will not- exceed

α; here

.9-VaR ≈ 30,000.

The /J-CVaR is the conditional expectation of

losses above the amount- α; here

.9-CVa-R. ≈ 34,000.

These measures disqualify the policy of maximis-

ing the expected yield as a fund manager’s ob-

jective function. No manager would accept- such a

high risk in controlling a pension fund.

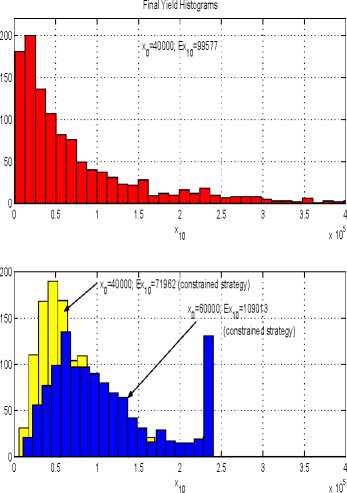

A different- strategy has to be considered. Sup-

pose that the manager will use a “constrained”

strategy: t⅛ιt = .5, U∙2,t = .02.τf (i.c., non optimal

with respect- to the expected value criterion). Wc

can see from Figure 21 (lower panel) that, for

the same initial outlay .τo = $40,000, the yield

distribution (represented by the light- histogram)

is more concentrated and less skewed than the

unconstrained one (upper panel). The mean for

this portfolio is $84,100 (mcdian=58,710) and the

standard deviation diminishes to $45,563 from

$168,000 for the unconstrained policy. The dark

histogram represents the final fund’s yield dis-

tribution for the constrained strategy applied to

.τo = 60,000. In this ease, the mean value is

Fig. 21. Fund yield spread.

$109,013 (mcdian=93,000) and the standard de-

viation $63,322. Overall, the risk of performing

worse than investing in the secure asset- alone is

much less under a constrained strategy. The risk

of scoring less than .τ0 is, for .τ0 = 40,000

.9-VaR ≈ 13,000 and .9-CVaR ≈ 17,000;

whereas for .τ0 = 60,000,

.9-VaR ≈ 21,000 and .9-CVaR ≈ 30,000.

Suppose now that the fund manager would like to

advertise their pension fund as paying an amount

Xτ for an initial outlay .tq∙16 It is clear from

the histograms in Figure 21 that an expected

value maximisation policy (constrained or not)

cannot- be used for this purpose. Instead, we will

examine the policy determined as a solution to

the stochastic optimal control problem with the

objective function given as

J(0,.τ(0)ρu) =IE ^7r(.ττ)∣ .τ(0) = .τo^ (37)

where

1 ( x ʃ (∙'fτ -⅛)5 if xτ > xτ■ ∕o8∖

This criterion reflects the manager’s wish to dis-

pose of sufficient- funds to meet- the target- xτ∙ At

the same time, it- docs not- prompt- the manager to

accumulate (much) more than needed.

15Soo [1] for a static portfolio analysis based on VaR and

CλraR.

10In other words, the manager will sell a ten year “bond7’

Sio fɑɪ' -ro-

ll

More intriguing information

1. The name is absent2. Opciones de política económica en el Perú 2011-2015

3. The name is absent

4. Evolution of cognitive function via redeployment of brain areas

5. On s-additive robust representation of convex risk measures for unbounded financial positions in the presence of uncertainty about the market model

6. Human Development and Regional Disparities in Iran:A Policy Model

7. Economic Evaluation of Positron Emission Tomography (PET) in Non Small Cell Lung Cancer (NSCLC), CHERE Working Paper 2007/6

8. The name is absent

9. Implementation of a 3GPP LTE Turbo Decoder Accelerator on GPU

10. The name is absent